Innovative Research / Groundwork Collaborative

Fixing Housing Means Fixing Finance: Why We Can’t Deregulate Our Way to Affordability

March 25, 2026

Overview

In this brief, we dissect the housing affordability debate, zeroing in on financing conditions that have largely been missing. We lay out the fundamentals of housing economics, survey the current policy landscape, and explain how popular proposals to loosen regulations may not lower housing costs on their own. And we outline the federal policy levers that would actually make housing more affordable.

I. Introduction

Housing is one of our most basic social needs, essential for physical comfort, social inclusion, and survival. The type of housing available to you can dictate the jobs you take, the cities you move to, the schools or other public services available to you, and the choice of whether to start a family.

For many families, housing constitutes a third of their entire annual budget, making it the single-biggest driver of the cost of living.1 Those making less than $30,000 a year can spend over 60% of their income on housing.2 Younger, lower-income families who tend to be renters or first-time homebuyers, are hit particularly hard.3 And sky-high housing costs in dynamic, high-wage metropolitan areas stifle economic mobility and suffocate growth, while exacerbating a zero-sum game where immigrants and other outsiders become competitors for scarce resources.

Housing is one of our most basic social needs, essential for physical comfort, social inclusion, and survival.

It’s no surprise, then, that affordability politics have long focused on the cost of housing. In the early 20th century, rent strikes and protests convulsed New York City.4 Thanks to a combination of vigorous homebuilding spurred by generous federal support and a population shift away from central cities, housing affordability became a less acute issue later in the 20th century.5 But affordability has once again grown in salience, thanks to lagging new-home construction and the cosmopolitan resurgence of many coastal cities.6

Since roughly 2012, when the U.S. housing market bottomed out after the Great Recession, affordability has been eroding as home values crept upward and then surged during the pandemic. From 2007 to 2017, the proportion of people in their 30s and 40s who owned their own homes fell by about 10 points, thanks to a weak labor market and slow income growth.7 Over the past decade, rents have risen by over 50% — slightly more than average hourly wages — and home prices have nearly doubled.8 In that time, the consumer price index has risen by only one-third.

To be sure, many forces were acting on the housing market following the Great Recession. While the returns to real estate collapsed in its immediate aftermath, in the years that followed tight financing conditions constrained housing production even when it became apparent that the U.S. economy had dodged a second Great Depression. This greatly contributed to the slow recovery in the construction sector. While there has been some recovery since the Great Recession, homeownership rates remain well short of the mid-2000s levels.10

Of late, the view that restrictive land-use policies are the most important factor in affordable housing availability has gained considerable purchase among academics and policymakers.11 In one example, economists Edward Glaeser and Joseph Gyourko argue in a series of papers that restrictive zoning and regulations prevent a sufficient number of new homes from being brought to market, driving up prices and rents.12 This view, often taken for granted by policymakers, is premised on the claim that land-use rules and other regulations — many of them allegedly superfluous — stymie supply.

This brief addresses the second of these claims — that excessive regulation is the main reason for insufficient production of new housing. We aim to examine the basic economics of rental housing and asset markets to explain why deregulation alone is highly unlikely to meaningfully or sustainably address the issue of housing affordability.

The number of homes available for sale or rent in a given metro area is, of course, a key factor in dictating housing costs. If one could snap their fingers and double the number of homes in one area, a la Marvel’s Thanos the Mad Titan,13 one should expect the cost of housing in that area to fall. But it does not follow that mere deregulation will substantially galvanize housing production.

We strongly support reforms to land-use rules to allow higher density. But it is unlikely that simply removing regulations and changing these rules will lead to improved and sustained affordability in a reasonable timeframe — desirable though these reforms may be on other grounds.

There are numerous possible explanations for the high cost of housing. Quantitative restrictions on the number of housing units that can be built are one possibility. Another is high building costs, which could stem from regulations or flagging productivity in construction. For rentals, one explanation could be the market power of incumbent suppliers. Since housing is a nontradeable good that relies heavily on labor, rising incomes are also a plausible cause for spiking home prices and rents.

But one important factor is largely absent from the debate: financing.

As an industry, housing is particularly sensitive to financing conditions. Builders are often small enterprises dependent on external funding. Surveys of executives and other empirical work on corporate investment suggest that interest rates have surprisingly little effect on most investment decisions, largely because corporations finance investment largely out of their own retained earnings.14 And small businesses, which are more likely to be credit-constrained, are responsible for relatively little capital spending. Housing developers are unique in their combination of dependence on external finance and large-scale capital spending.

More than almost any other major industry, builders depend on outside investors for project financing. What’s important to understand is that the returns they anticipate come not just from current rents, but from an expectation of rising rents. Those rising rents, in turn, are eventually capitalized into building values, accruing as capital gains. This central fact about housing explains both the instability of construction spending and why land-use reform, on its own, is unlikely to deliver substantially lower housing costs: When the rent drops, the building stops.

In this brief, we dissect the housing affordability debate, zeroing in on financing conditions that have largely been missing. We lay out the fundamentals of housing economics, survey the current policy landscape, and explain how popular proposals to loosen regulations may not lower housing costs on their own. And we outline the federal policy levers that would actually make housing more affordable.

Fixing Housing Means Fixing Finance: Why We Can’t Deregulate Our Way to Affordability

Housing is a fundamental human need; in the modern United States, access to housing shapes people’s

life chances and capacity to contribute economically in far-reaching ways. But from the point of

view of the investors who finance it, housing is an asset. This means that as long as we are dependent

on privately financed developers to supply the great bulk of our new housing, the sector must offer an

acceptable return.

Read the Full Report.

II. The economics of housing development: Private developers will only build housing when it offers an acceptable rate of return

To understand housing finance in the United States, it’s important to first recognize that investors view housing as an asset. To draw private financing, home construction must generate returns to its owners, either through rental income or by appreciation. Both developers and investors weigh this fact when making decisions in the housing market.

As with most other rich countries, in the United States private developers produce almost all new housing — and they do so for a profit.15 This is, of course, true of many other critical industries, such as food or energy. But the housing market is distinct from other markets in two important ways.

First, private businesses carry out most housing development, with the help of outside financing. Second, homes are long-lived assets, meaning that the reward to the builder depends not just on the price of housing today, but its expected price in the future.

For an investor weighing whether to put money into producing a building or some other long-lived asset, the decision comes down to the expected returns. Returns can be realized in two ways: An asset can produce income or cash flow, or it can appreciate in value over time. For a real estate investment to be worthwhile, either home or land values must go up, or real estate must generate income for its operators in the form of rents (or some combination of the two).

In real estate-industry jargon, the net income produced by a property is expressed as the capitalization rate, or “cap rate.”16 Think of it like a bond yield or stock dividend yield: It’s the percentage return a property generates for its owners for the act of owning it, exclusive of any appreciation. Cap rates are calculated by dividing yearly net rental income by the building’s value or cost to construct. Cap rates play a critical role in how real estate investors decide whether to purchase or construct rental housing.

We can infer property values17 by flipping the concept of the cap rate on its head with a common valuation method known as “rent capitalization.” In essence, the price or valuation of any apartment building is just an extrapolation of the net income stream it is predicted to produce. As will become apparent, the role of capital gains, derived via rent growth, is key to making housing “pencil” — that is, to ensuring it can clear the required hurdle rates that private investors demand given the risk and illiquidity of real estate investments.

Housing finance: A mix of equity and debt

The core of housing finance is what’s known as a “capital stack:” the specific blend of equity and debt required for a given project. Before undertaking a project, private developers require a certain level of return.18 The size of that return is determined both by the returns required by individual components of the capital stack, and by the proportions of each.

Here’s how it breaks down. So-called “senior debt” will carry an interest rate linked to prevailing interest rates, which are strongly influenced by federal monetary policy. “Junior,” or mezzanine debt, carries a higher rate. Equity investment, while less sensitive to prevailing interest rates, requires the highest rate of return. Construction finance also requires a higher rate of return than that required to purchase an existing building.

Suppose19 a project was financed with 40% equity, 40% senior debt, and 20% mezzanine debt. Let’s assume the equity investors expect a 20% rate of return, the senior debt carries a 5% interest rate, and the junior debt carries a 15% interest rate. Under that scenario, the project as a whole would have to generate a return of 13% to be viable.20

Typically, this return would be achieved over the first five years of the project. After that, sale or refinancing would allow for the initial equity investors and lenders to be paid off. Then, a new mortgage would be incurred on more favorable terms21 since it would now be financing a completed, rented-out property rather than a speculative construction project.

The broad asset market binds housing production

Investors view housing as an asset with a rate of return. As a result, the sector competes with other potential investment vehicles — stocks, bonds, or so-called “alternatives” like private equity and hedge funds — for investment dollars.22 To attract these investors, including large institutions such as pension funds or wealthy individuals, projects must offer returns they regard as at least as good as the next best alternative, adjusting for risk.

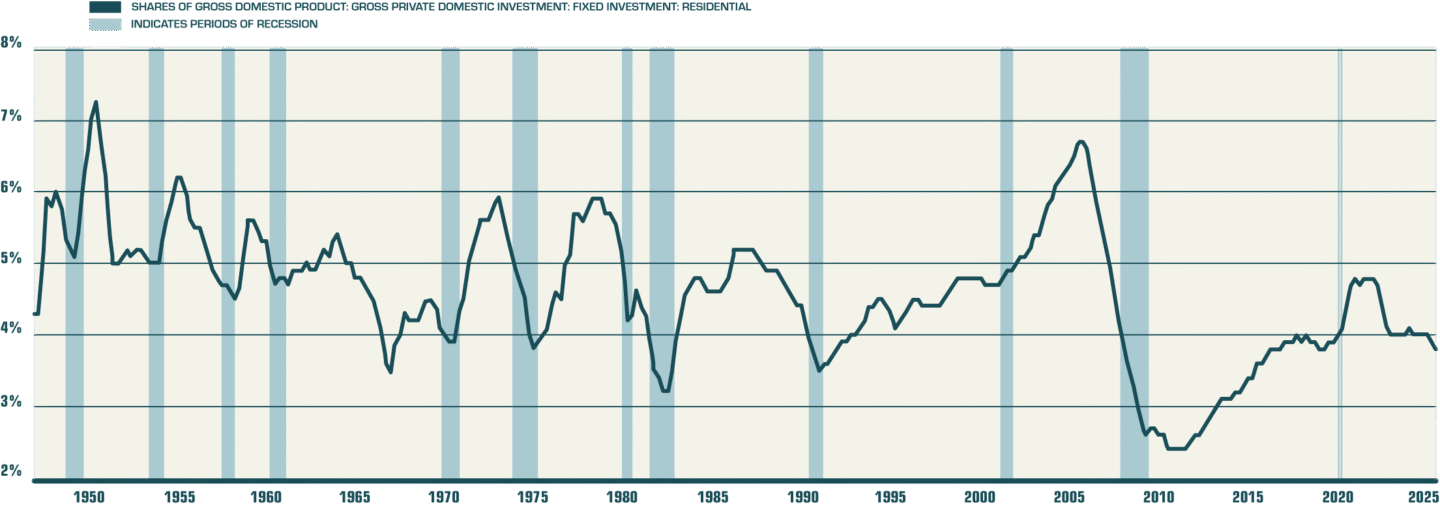

Since construction is inherently risky and investor expectations about returns frequently shift in the housing market, investment in residential construction as a percent of GDP is highly volatile.23

Source: U.S. Bureau of Economic Analysis via FRED

To further complicate matters, because investors are extremely sensitive to changes in potential returns, and returns to housing tend to fall as supply increases, housing starts are highly volatile and “self correcting.”24 When rent growth is strong,25 returns to rental housing tend to be high, which attracts investment and can spur the building of new units.

But as new completions hit the market, rent growth flattens and housing starts fall sharply. This exact dynamic played out during the recent supply response to the rent surge in 2020 to 2022. Starts for apartment buildings reached a 50-year high.26 Then, as rent growth flattened in 2023, starts fell precipitously.27

As noted above, the real estate sector is also highly sensitive to changes in interest rates. Increasing interest rates have also contributed to the fall in housing starts since 2022, especially since the Federal Reserve’s most recent tightening has — unlike in the previous two cycles — quickly sent mortgage rates spiking.28

Without leverage, rental housing does not offer very attractive returns to investors.29 Yet, real estate is a tradeable asset that serves as strong collateral. As a result, banks and other lenders willingly lend against it. When lending rates in the real estate sector are below cap rates and substantially below total returns, it is possible to use leverage to substantially increase returns to equity well above the industry’s benchmark 20% internal rate of return (IRR). However, as interest rates rise, and, crucially, if lending rates are close to or even exceed total returns, taking on additional leverage can decrease returns to equity, stalling development.

For all these reasons, housing is subject to exceptionally large cyclical swings. In recessions, the fall in residential investment is typically larger than the fall in nonresidential investment or consumption despite the fact that those latter components make up a much larger share of the total. It is with good reason, then, that the economist Edward Leamer, in a widely quoted article, argued that “Housing IS the Business Cycle.”30

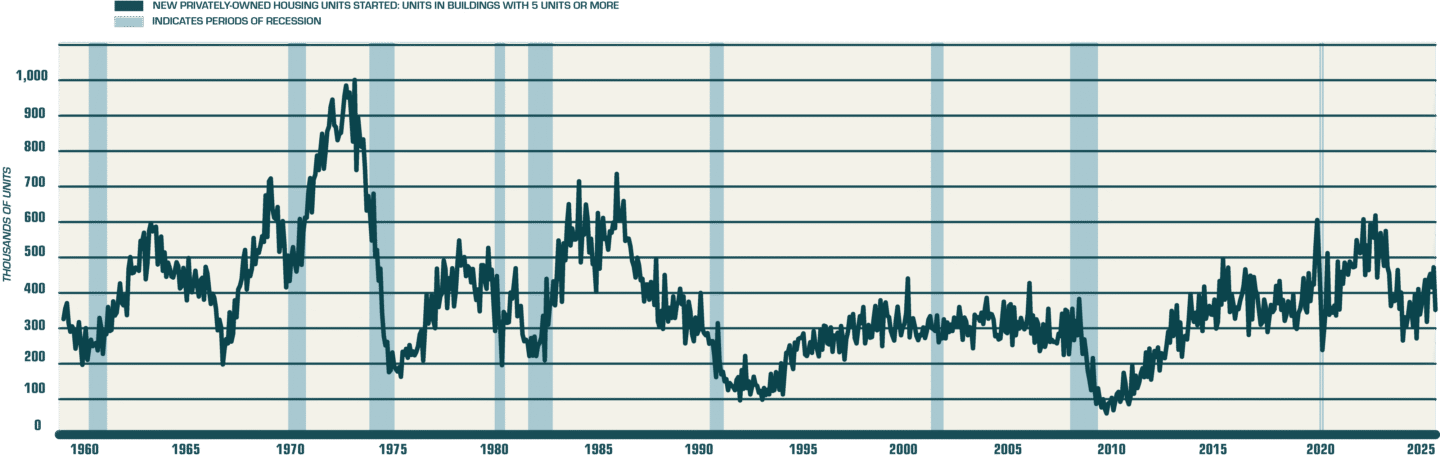

Source: U.S. Census Bureau; U.S. Department of Housing and Urban Development via FRED

Rent growth is key to attracting private investment in housing

Many families struggle to keep up with ever-rising rents. Yet rent payments themselves do not generate the bulk of the returns for most existing or newly constructed rental housing.31 Because of high construction costs relative to market rents, starting (or “going in,” in real estate parlance) cap rates for owners have, historically, remained within a tight range of four to eight percent annually — substantially below typical hurdle rates for real estate investors.32

To augment returns from rental yield alone, then, investors need asset prices to appreciate. But buildings are typically valued as a multiple of their net rental income. So, for investors to receive their capital gains, rents must rise.

This is why investors, when deciding where to build, examine recent trends in the rental market. If a particular area shows no history of strong rent growth, builders are unlikely to supply much new housing there since the rental yield alone will fail to deliver adequate returns given the risks. Aging industrial centers in the Midwest like Kalamazoo, Michigan, and smaller metro areas in general like Tulsa, Oklahoma, tend to fall into this category. While these cities certainly have existing rental markets, it’s usually not viable to build new housing projects that depend on rent growth to deliver sufficient returns given the risks.33

Naturally, new housing supply coming on the market pushes up vacancy rates, which, in turn, puts downward pressure on rents as projects attract occupants.34 This causes investors to quickly pull back investment, kicking off a new period of little new housing — and rising rents.35

Many mistake short-run rent declines or deceleration of rent growth as proof that permissive zoning will enable investors to build to affordability. The reality is that the market is unlikely to sustain a level of building which could cause a long-term secular decline in rents — or even substantially slower rent growth — precisely because that environment would not offer high enough returns to investors. These cycles of investment and rapid disinvestment will almost never result in long-run improved affordability.

Zoning is not a “hard cap” on housing production

So-called YIMBYs (Yes In My Backyard) tell a basic “quantity” story in housing-policy debates: Regulations constrain the number of houses that can be built, creating supply scarcity, which drives up prices and rents.36 As a solution, YIMBY groups advocate almost exclusively for permissive zoning and building-code reform to tackle housing affordability.37

This view correctly identifies a substantial part of the problem. But it offers an inadequate solution.

If it were true, as YIMBYs generally attest, that zoning regulations represented a hard cap on the number of housing units in a given city, we would expect that the value of existing buildings would be substantially higher than the potential development costs of new projects if they were allowed to go forward. Following that logic, existing building owners would hold such extreme, almost monopolistic market power which would get capitalized into building values. As such, we would expect existing building values to be above the cost of new development in cities with restrictive zoning, again, if new development was allowed to proceed.

Under such a scenario, we would see new development in these cities even if rents were flat or falling because the development costs of new buildings would be low relative to high market rents. Rental yields or cap rates for new projects would be so high — potentially exceeding 20% — that projects would no longer rely on capital gains to clear hurdle rates. Or, conversely, new development could be constructed at substantially lower rents (because of low building costs relative to existing building values) than existing market rates, which would put strong downward pressure across the entire rental market.

People who see land-use reform as the panacea for housing costs implicitly take this as the norm: If regulations impose hard ceilings on the amount of new housing produced, then, indeed, it would be possible to construct new buildings at a cost significantly below the value of existing ones.

But, in actuality, there are few if any areas in the U.S. where this is happening.

Even in New York City, which suffers from one of the nation’s most acute housing crises, a recent study found that even existing zoning restrictions would allow an additional 390,000 housing units to be built as of right now (and another 190,000 in nearby Westchester County and Long Island).38 While this may not meet the city’s long-term needs, it is still considerably greater than its total housing additions over the past 15 years.39 This suggests that in much of the New York City metro area, land-use rules are not the binding constraint on new development: There are many areas where new housing is permitted, but because private developers do not expect it to be sufficiently profitable, in their eyes it’s just not worth building.

Even in one of the country’s highest-rent metro areas, profitability, rather than zoning, is a more important constraint on new construction.

Could development move forward without expected rent growth if building values were significantly higher than development costs (inclusive of the risk associated with all major construction projects)? In principle, yes. Developers could still make adequate returns by constructing new projects at costs below existing building values and then sell them to investors.

But this is plausible only in a setting where land-use rules (or some other factor) impose a hard cap on the number of new buildings that can be constructed. Otherwise, we would expect to see a convergence between the cost of new construction and the price of comparable existing buildings. (Of course, adjusting for the risk of new construction and building age/condition).

And since even very high-cost cities are not built out to allowable density under existing rules, there is little reason to believe that zoning is acting as such a hard cap on the number of housing units.40 In general, building values even in high-cost cities are not higher than development costs. And even if they are in certain cities — or, more likely, in sub-markets within large metros — such a situation is hardly generalizable to the country as a whole, which has seen a nationwide erosion of housing affordability. In almost all of the country, including most areas close to high-cost cities or within them, the binding constraint on new construction is expected returns.41

As long as housing is built and financed by for-profit developers, the expected returns on a project will be a critical constraint on whether it goes forward — and expected rent growth is often the largest part of those returns. In an environment of slower, zero, or negative rent growth, many fewer projects will be attractive to private developers.42

In the vast majority of housing markets, relying on private capital to “build to affordability” is simply incompatible with the underlying math of generating required returns — as long as housing is built by privately financed for-profit developers.

III. Our inadequate policy landscape won’t solve the housing affordability crisis

Upzoning and building code reforms are an important part of the housing policy package.43 There are many central areas — both in metropolitan cores and smaller cities — that have sufficient transportation and other infrastructure to support substantially higher levels of housing density, and in many cases higher than current regulations allow.44 Increasing the number of people able to live in dense urban areas has a wide range of economic, environmental, and cultural benefits.

For all these reasons, we welcome a world in which more people live in dense urban areas. But at present, many people who would benefit from doing so cannot, due to a lack of affordable housing.45 While many elements of land-use regulation and building codes reflect genuine health and safety concerns, others have not kept up with changing construction techniques. In other cases, they impose an excessively narrow view of the kind of housing worth building.

On all of this, we agree with the YIMBY position.

But we dispute the idea that land-use reform can substantially reduce housing costs, in the absence of complementary reforms that would allow development to proceed at substantially lower returns than investors require today.46

In this section, we will offer constructive critiques to the so-called YIMBY movement, drawing on the foundation we established in the first section.

Building Code Changes and Easing Construction Requirements

New buildings must fulfill numerous requirements. Building codes require minimum safety standards.47 Oftentimes, rules require parking spaces.48 All these rules or requirements add to building costs.49 For example, one unit of structured parking can increase per unit costs by an average of $50,000, with costs climbing even higher when garages are built with multiple levels or underground.50 If occupants cannot absorb them in the form of higher rents, this will harm returns and reduce housing production.51

Some of these changes, when made thoughtfully and without undermining safety, can result in non-trivial savings. These changes offer one-off reductions in building costs that can be significant in the short run. However, in the long run, they may fail to impact affordability.

At present, the most optimistic estimate for how much regulatory changes could increase affordability is around 20% of total building costs. Unfortunately, even under this rosy scenario, long-term affordability may not be impacted much.

Two possible outcomes (which are not mutually exclusive) would result from such cost savings. If building costs fell by 20%, rents could fall by 20% and maintain the prevailing rental yields needed to support new construction. Of course, new construction could still only proceed if projected rent increases are sufficient to deliver adequate capital gains. But this is likely to outpace wage growth, thus, any one-off gains to affordability would be reversed by long-term rent increases.52

Another possibility would be for none of the cost savings to be immediately passed on to renters in the form of lower rents. Instead, higher going-in rental yields would enable projects to be developed with lower rent growth projections. This has the advantage of bending the growth curve for rents. But depending on wage growth, this may only slow the speed at which housing becomes unaffordable, rather than actually improving affordability.

To be clear, both these outcomes are directional improvements from the status quo. We only wish to demonstrate how savings from regulatory changes alone, even when substantial, are inadequate to fully address the current crisis of housing affordability.

Lower costs will likely spur new construction, bringing down market rents or slowing rent growth. But while this is good news for tenants, these lower costs are unlikely to produce major gains to affordability. And to the extent they do so, it is likely to be through extended boom-and-bust cycles where developers respond to cost reductions by initially overbuilding, and then pulling back.

YIMBYism is most commonly associated with allowing denser construction modes in a specific area, or what’s known as upzoning.53 YIMBYs contend that reserving too much land for low-density construction constricts the number of housing units that can be built, raising housing prices.54

Building-code reforms involve complex tradeoffs between construction costs, health and safety standards, environmental concerns, and the legitimate interests of workers, in ways that make it challenging to deliver major cost reductions without sacrificing other important social goals. Upzoning, by contrast, is conceptually straightforward, and does not require the same kinds of tradeoffs.

Upzoning is certainly within the power of state and local governments. It may well increase the number of units built relative to the counterfactual. There is a strong case for allowing higher-density development in much of the country. But there are reasons to be skeptical about whether upzoning, on its own, will meaningfully impact affordability.55

First, high-density construction modes are typically more expensive per square foot than low-density modes like single-family homes. As a result, upzoning leads to more housing units only if occupants pay substantially more per square foot in rent. This is because unless rents rise per square foot, the increased costs will simply lower projected returns, which would either stop building entirely or heavily incentivize lower-density building.56

In many desirable parts of the country, tenants willingly pay substantially more per square foot in rent (or to buy homes) in exchange for proximity to high-paying jobs, places of cultural significance, or attractive amenities. But the reality is that the market rents or prices per square foot in most places currently zoned for single-family housing would not support higher levels of density. Minneapolis eliminated single-family zoning, yet most neighborhoods did not experience rapid redevelopment or any redevelopment at all.57 Rents in San Francisco have been relatively flat since 2019 — so potential returns, even given the city’s high level of rents, remain unattractive.58 Thus, if market conditions are not sufficient to induce investment, upzoning will not automatically result in a construction boom, even in high-rent areas.59

The more fundamental problem with efforts to use upzoning as a tool for affordability is that, with only a few exceptions, the binding constraint on development is profitability. Almost all housing markets contain substantial amounts of land where additional housing could be built under existing zoning rules, but expected returns are not high enough to incentivize developers to do so. Even moderately slower rent growth can substantially reduce expected returns. In a setting where development is constrained by profitability, lower expected rent growth will mean that many projects will no longer promise sufficient returns to go forward.

For this reason, we would expect upzoning to deliver sustained growth in housing production only in settings where housing demand is strong enough — or more precisely, elastic enough — that more rapid growth in the housing stock does not cause rent growth to slow. Again, there are many reasons why allowing more people to live in dense urban areas is desirable in and of itself, independent of affordability. But a sustained fall in housing costs will require tools beyond upzoning.

IV. Policy implications and solutions

Slowing the growth in housing prices, then, will require developers to take on projects at significantly lower expected returns than they currently require. Of course, this is not to say that new housing is never built in an environment of stable or falling rents. Investors are often mistaken about the future. And optimistic beliefs about future returns are common in speculative markets like housing, because of the long lag between commitment to a project and the date when returns are realized.60 By the time it’s clear that the expected rent growth isn’t coming, the project may be too far along to halt. These kinds of investor errors and speculative dynamics can, at best, deliver brief housing booms. But they can’t deliver the steady supply growth necessary to slow growth in housing costs. That would take investors accepting returns lower than what the market currently requires.

As long as for-profit developers produce the vast majority of new housing, any policy that is likely to lower returns on new housing must also reduce construction or financing costs to ensure that investment in new housing continues. But substantially lowering construction costs is very difficult; slow productivity growth in construction is a long-standing, intractable problem.61 Regulatory reforms, meanwhile, are unlikely to lower construction costs enough to meaningfully affect housing prices without unacceptable tradeoffs on safety and environmental standards (and perhaps not even then).

By comparison, reducing financing costs is more straightforward. In an environment of slower rent growth, this is the key to sustainable private production of housing.

Historical Models

Historically, the U.S. has seen extended periods of adequate housing production only when financing conditions for new development allowed projects to go forward at significantly lower returns than they currently require. Modern U.S. history offers at least two main ways of achieving this: specialized housing lenders, such as thrifts or Savings and Loan associations, and subsidies to developers, either through the Department of Housing and Urban Development or accelerated depreciation for housing in the tax code.62

We propose a third approach: public sector junior or mezzanine loans to developers.

The underlying logic: The public sector should never hesitate to invest when there is a need and the private sector won’t provide. A federal public housing loan program could allow housing-development projects to advance at lower returns, without any net cost to the public. The government could lend to housing developers at a rate low enough to significantly improve their financing terms, while still greater than the government’s own effective cost of funds. A particular appeal of this model in the present moment is that it could be pursued by state and local governments — not only at the federal level.

Today, developers are competing for financing with the full range of other investments. But for much of U.S. history, this was not the case.

One important piece of this partitioned financial system was the Savings and Loan associations (S&Ls), or thrifts, among the most important sources of housing finance through most of the 20th century.63 From the 1930s to the early 1980s, thrifts, a product of New Deal banking legislation, offered low-cost financing for new housing development. S&Ls were often the only financial institution permitted to accept deposits in a given community, due to strict limits on bank branching.64 And the prohibition on interest payments on checking deposits (and on the use of other types of deposits for payments), along with the limits on interest rates on other types of deposits, meant that S&Ls benefited from very cheap deposit financing on their liability side.65

At the same time, S&Ls were strictly limited in the types of investments they could make on their asset side — essentially, they could lend only for local real estate projects. Rather than allowing household savings to flow into an undifferentiated national capital market that forced housing developers to compete with all kinds of other investments, there were a large number of small, walled-off capital markets where local savings could flow only to local housing development. Meanwhile, business investment was largely financed through the retained earnings of existing businesses, rather than through capital markets. Creating this pool of captive finance for housing investment was an explicit goal of New Deal banking legislation.66

By the mid-1960s, S&Ls held 26% of consumer savings and provided 46% of all single-family home loans.67 As of 1980, the $480 billion in mortgage loans originated and held by the sector represented half of the $960 billion in home mortgages outstanding at that time.68

In the 1980s, the sector entered terminal decline. Reagan-era financial deregulation opened thrifts up to competition from institutions offering higher returns to depositors. To compete, S&Ls had to offer higher returns themselves, forcing them to turn from residential mortgages to speculative commercial real estate projects — a move also encouraged through deregulation.

The end result of this was the spectacular failure of many of these institutions, and the absorption of the remainder into the larger banking system.69 The postwar model of specialized institutions providing cheap housing finance could only survive in an environment of comprehensive financial regulation.

In effect, the post-New Deal banking system offered more favorable financing terms for housing and greater financial stability and support for local economic development, at the cost of lower returns for small savers and less financing for new investment outside of established businesses.

Whether this tradeoff was, on balance, worth it, is beyond the scope of this paper. And in any case, this regime was the product of particular historical circumstances that could not be recreated today.

But this history explains why it was once possible to sustain a level of housing investment on pace with family formation, leading to a relative decline in housing costs. Between 1950 and 1980, rents rose by about 30% less than the consumer price index as a whole, compared with their 50% greater increase over the past decade.70 The rise and fall of thrifts also suggests a goal or general direction for housing policy: It will be easier to build housing without rising rents to the extent that housing finance can be separated from the larger financial markets.

Today, in the absence of a comprehensive re-regulation of financial markets, it is hard to imagine how we might create a similar walled-off pool of housing finance. One alternative approach: subsidizing housing development, which would lower the effective cost of finance and — crucially — the required returns.

One of the most ambitious attempts to do this in the U.S. was Section 236 of the Housing and Urban Development Act of 1968, which created a new program of subsidies for mortgages for multifamily housing development.71 Under Section 236, participating projects would receive a sufficient subsidy to reduce the effective interest rate on the mortgage to as low as one percent.72 In return, rents for future tenants were capped at a level sufficient to recover operating costs and the (subsidized) debt-service payments.

While the program was only in operation for five years, it appears to have made a significant contribution to new housing development.73 The period 1972 to 1973, the program’s final year in operation, saw the highest number of multifamily housing starts (as well as the highest level of overall housing starts) in U.S. history.74 While numerous factors contributed to the boom, Section 236 made an important contribution. Between 1970 and 1973, approximately 400,000 new units of affordable housing were started through Section 236 — more than 10% of the new rental housing built during this period.75

In 1974, Section 236 was replaced by the Section 8 New Construction and Substantial Rehabilitation program, also known as the project-based Section 8 program.76 This, in turn, was phased out in 1983, replaced by vouchers to individual tenants, which are generally less effective at achieving housing affordability than supply-side interventions.77 This is because when supply is inelastic, supporting demand through vouchers tends to raise the market price. In effect, this means that much of the benefit is captured by landlords, not tenants.

The 1981 tax bill, which offered accelerated depreciation on new housing investment, suggested a different approach to subsidizing housing development.78 In effect, development of new housing received a subsidy in the form of lower tax liability for developers in future years.79 These subsidies were larger for low-income projects. According to the Tax Foundation, “the 1981 tax reform significantly reduced the cost of capital” for new housing development.80 Economic studies have suggested that the 1981 tax law was a major factor in the boom in multifamily construction during the early 1980s, and that the reversal of these provisions in 1986 helped bring an end to that boom.81 While the 1981 law may have stimulated construction, it also led to massive revenue loss and created huge windfall gains for developers on countless projects that likely would have gone forward in any case.82 So while the 1981 law is not a model for housing policy today, our point is that, historically, the U.S. has seen periods of exceptionally strong housing development when policy changes have effectively reduced financing costs for developers.

The two periods in modern U.S. history that saw the greatest amount of new rental housing built were 1971-1973 and 1982-1986.83 Both of these periods directly followed the introduction of policies to reduce financing costs for new housing, and ended as soon as those policies were phased out. By contrast, it is hard to associate historical booms and busts in housing construction with changes in land-use rules.

The implication of this history is that for sustained construction on a scale sufficient to generate sustainably lower rents, it will not be enough to simply permit more housing to be built, especially in the majority of the country where land-use rules are not the binding constraint on construction. It is essential to allow housing to be built at a lower expected return than developers currently require, something that, in the long run, might be best achieved by moving toward a public, social, or nonprofit model of housing development. For the near term, the great majority of housing will continue to be built by for-profit developers. Under these conditions, the way to allow homebuilding to go forward with lower expected returns is to reduce the cost of housing finance.

Expected returns to housing, and the returns housing offers relative to other asset classes, is the main constraint on housing-market production. Investors in housing expect very high returns, given the sector’s risk and illiquidity; any solutions must contend with this reality. Policies to increase housing production must, then, either augment returns or change the terms of housing finance so that projects with lower expected returns are viable. In an economy that depends on market-financed for-profit developers for new housing production, no policy that fails to address this side of the problem can succeed at scale.

Adding public funding to the capital stack

To sustain new housing development in an environment of slower rent growth, policies are needed to reduce the return acceptable to developers. There are a number of models available to do this, all of which involve offering financing on terms that private investors will not.

Public lenders do not have to be bound by the same standards as private lenders. Adding additional public lending to the capital stack can reduce the high-cost equity funding required. And if these public loans are subordinate to those from private lenders, they will not affect the project’s ability to obtain private financing.

Because of the very large difference in returns expected by equity investors and prevailing interest rates, public loans that allow projects to go forward with less equity will substantially bring down the overall required return on new housing projects. This means that public lenders do not need to lend at concessionary rates if they are willing to accept a lower share of equity — and thus bear more of the risk — than private lenders would. In the extreme case, the public sector can replace equity investors entirely, as the Montgomery County Housing Production Fund has in some projects, for example.84

In addition to reducing the costs of new housing development and making projects viable even in an environment of slower rent growth, public finance of housing has another crucial benefit: It’s likely to make housing development less cyclical. In the contemporary United States, large boom-and-bust cycles in housing production have substantial costs, both macroeconomically and for the millions of people who depend on construction of housing for their income. Public lenders can not only offer financing on more favorable terms than private lenders: They can also do so on more consistent terms, while offsetting fluctuations in expected returns. This is the opposite of private lenders, who are inclined to lend for housing development at times and in areas where development is already strong.

At the federal level, a natural vehicle for reducing the financing costs for housing development are the government-sponsored entities (GSEs) Fannie Mae and Freddie Mac, though many other approaches are possible. At the state and local level, there are already a number of experiments with housing loan funds, that could be expanded.

Are public loans just subsidies?

A subsidy to spur housing production is almost always a better use of public money than a subsidy to a renter or homebuyer. A basic principle of economics is that the incidence of a tax or subsidy on some purchase depends on the elasticities of supply and demand: The more inelastic the supply, the more the tax or subsidy will fall on producers rather than consumers. The short-run supply of housing is very inelastic. This means that subsidies to renters or home purchasers mainly benefit owners of existing housing by bidding up the price, so the benefits to renters are less than the public money spent — and renters who don’t get subsidies may even be worse off.

Conversely, subsidies to new housing construction not only have direct benefits for whoever lives in the additional housing. They have the further, indirect benefit of pushing down market prices for housing in general. Just as a tight labor market increases competition among employers, leading to better wages and working conditions for employees, additional new housing construction increases the bargaining power of renters and new homebuyers relative to owners of existing housing.

But public lending need not be a subsidy — it need not impose costs on the public sector. There are good reasons why the public can accept lower rates on construction loans than private lenders will.

For one, the public sector itself can borrow very cheaply. New York City is currently issuing general obligation bonds, a type of municipal bond backed by the “full faith and credit” of the issuing government, at rates between 3.1% and 4.87%, depending on the maturity of the bond.85 Given the double-digit rates typically carried by mezzanine loans, a government could issue bonds to fund construction loans at much lower rates than what private lenders offer, while maintaining a comfortable cushion above its own cost of borrowing. The low borrowing costs, in turn, reflect the favorable tax treatment of municipal bonds, along with the size and stability of the public sector. There is a clear economic logic for the public sector to bear more risk and use its own financial strength to support borrowers in sectors where credit constraints are an issue.

There are yet other reasons why the public sector is particularly well-suited to finance housing construction. One of the fundamental economic facts about housing is that it is very long-lived. For investors, by contrast, the horizons are relatively short. Assets that will continue to produce benefits many decades from now will be systematically undervalued by investors who must evaluate their returns over a few years, at most. The focus on short-term returns by equity investors like private-equity funds is the unavoidable result of structural conditions.

Public entities are better positioned to focus on the long term. They do not have shareholders or other investors to whom they must make payouts, or report quarterly results. Nor do they need to demonstrate high returns on their investments in order to attract new investors; it’s sufficient that the loans, net of defaults, generate enough income to repay their own borrowing costs.

Public entities can also trade debt for equity. Where delays or unexpectedly high costs prevent developers from meeting their debt commitments, a public lender can take an ownership stake instead. This model is also important in financing for existing buildings, where distressed owners often prioritize debt service over essential maintenance and repairs. Public lenders can offer debt relief in exchange for commitments to maintain habitability.

Furthermore, new development projects would grow the state and municipal tax bases, meaning that total returns after considering these effects may be significantly higher than underwritten project returns. In this sense, a public lender is able to internalize the positive externalities of new housing construction.

A larger role for Fannie Mae and Freddie Mac in multifamily housing

At the federal level, a natural way to reduce the financing cost of new multifamily housing is via Fannie Mae and Freddie Mac, two large government sponsored enterprises (GSEs) that purchase mortgages for multifamily and residential buildings in the secondary market. The loans they purchase are not construction loans, but loans incurred to finance acquisition of already-built and operating structures. But while these purchases may help support the market value of existing housing assets, they have, at best, a weak and indirect effect on new construction.

GSE purchases would have a much greater impact if they included construction loans, especially junior or mezzanine loans that would get repaid after senior debt.86 The greater risk of these loans from the point of view of lenders makes them more costly for developers. It also means that the guaranteed market offered by the GSEs would have a greater impact.

Jim Millstein, an attorney, financial executive, and senior Treasury official in the Obama administration who oversaw the AIG bailout, has proposed that the GSEs buy and securitize mezzanine loans to construct multifamily housing.87 Having the GSEs take a junior position in the debt would not change the terms or conditions that traditional lenders like banks offer developers, since banks would still be first in line to get repaid. It would, however, greatly reduce the amount of equity developers would need to raise before they start construction, which is typically the most costly — since it’s the riskiest — and hardest form of capital to raise. Even more importantly, since the mezzanine debt is junior to equity, any appreciation and net income would now be distributed among fewer equity investors, thereby raising the returns on investment for each individual investor. In sum, under the Millstein Proposal, not only would developers need to raise much less equity, their sales pitch would be much stronger since they could credibly promise much higher returns.88

In addition, since returns would be so much higher for equity investors, this structure would massively expand the feasibility envelope for potential projects. Projects delivering lower rents and lower rent growth would still be feasible because the profits and appreciation, though lower, would ultimately be divided between fewer investors. Millstein himself has even asserted that 100% affordable buildings rented to tenants at 30% to 80% AMI would still be attractive to many investors without further subsidies.89

This proposal holds tremendous promise because private mezzanine construction lending does exist, but typically at ruinously high interest rates above 15%, which only the most promising projects could ever hope to pay. By substantially lowering financing costs, this proposal expands the envelope of viability substantially and would allow more projects to proceed.

Additionally, the Federal Home Loan Bank (FHLB) System, a lesser-known GSE, could also play a larger role in financing housing construction.90 The FHLB system is a network of 11 government‑sponsored regional banks created by Congress in 1932 to support housing development and provide liquidity to its members (i.e, commercial banks, credit unions, community development financial institutions and insurance companies). As of June 2025, 93% of all banks were members.91 FHLBs are required by law to fund affordable housing initiatives targeted to certain income levels through grants, subsidies, or advances (loans) to member institutions, but over the last several decades the FHLB system has strayed from its original mission to also support financial institutions engaged in non-housing lending.92

Though it operates multiple programs to accomplish its goal of facilitating housing projects, one in particular — the Community Investment Program (CIP) — has untapped potential to help developers bridge financing gaps for new housing projects.93 By providing lower cost loans as well as issuing letters of credit that member institutions use to collateralize payments to third parties, CIP can increase the pool of capital available for constructing new housing. Unfortunately, the program is severely underutilized: In 2022, CIP was responsible for less than 0.1% of total FHLB advances, or just $3.5 billion out of $819 billion total.94 That same year, less than 175 of the nearly 6,500 FHLB members obtained CIP advances.95 For 2024, FHLB issued $4.9 billion in CIP advances, which funded just 4,411 rental units and 16,595 units for owner-occupants.96

In addition to using its existing balance sheet and programs to lower the cost of development, Congress should authorize FHLB advances to take a junior repayment position instead of a superlien position as they currently do.97 Additionally, FHFA can require that full savings from lower rates on FHLB advance be passed-through from member banks to housing developers.98 These reforms would further reduce the cost of capital for housing developers in need of financing.

State and municipal financing

Multiple states and localities have experimented with a variety of mechanisms for financing public and private housing development. The specifics of these programs are beyond the scope of this brief, but the Center for Public Enterprise, which works extensively on public financing for housing, as well as other forms of public investment, has a useful overview of what makes such programs successful.99

For our purposes, what’s most important is that public entities make loans with lower interest rates, long maturities, and more flexibility than private lenders. And they must be willing to make loans for construction — the riskiest and highest-cost segment. Bridge loans for projects that have used up their initial financing but are not yet fully leased up and able to shift toward more permanent financing, are also valuable.

One model for this kind of public housing finance is “housing accelerator funds” that provide subordinated loans to construct or rehabilitate housing.100 Many state housing agencies already issue tax-exempt municipal bonds which are repaid with mortgage payments collected from the projects the agencies finance.

Massachusetts has issued roughly $25 billion in such bonds since 1970 to help finance affordable housing. Recently, the Bay State authorized a massive expansion of its affordable housing financing program. In 2024, it authorized an additional $5.1 billion of new financing for housing projects, funded mostly via general obligation bonds.101 The state hopes to deploy this money over the next five years, which is a significant acceleration in the disbursement of state housing funds. Crucially, these programs can fill the gap in financing for needed projects that the private market is unwilling or reluctant to fund because of very high required returns.

Another model is the kind of revolving loan fund for housing established by Montgomery County, Maryland. As discussed in a report from the Center for Public Enterprise, this model was to issue long-term municipal bonds to create initial funds for a pool that is then used to make short-term construction loans.102 The interest and principal on these loans comes back to the pool once the projects are leased up, funding additional loans. In the Montgomery County case, the revolving loan fund has been used not only to support private housing development, but also to replace equity investors on fully public projects, allowing for the development of publicly owned housing without federal subsidies.

Many opponents of these initiatives worry about excessive public-sector indebtedness. However, public debt issued to fund housing projects will also create a revenue stream for the state as the loans funded by bond proceeds are repaid. In this sense, net indebtedness, after accounting for the loan repayments, will likely fall because housing projects will surely produce greater returns than the interest on tax-exempt municipal bonds. To be sure, some projects will fail, just as not all investments in a large portfolio pan out. However, aside from increasing housing production, such programs have the potential to be a profit center for state and local governments.

V. Conclusion

Housing is a fundamental human need; in the modern United States, access to housing shapes people’s life chances and capacity to contribute economically in far-reaching ways. But from the point of view of the investors who finance it, housing is an asset. This means that as long as we are dependent on privately financed developers to supply the great bulk of our new housing, the sector must offer an acceptable return.

The problem this poses for policy is that returns on housing investment depend on steadily rising rents. A policy that simply encourages the construction of more private housing — for instance, by relaxing land-use restrictions — may initially spur substantial new housing investment. But this is unlikely to be enough to lower housing costs in the long run. Once rents begin to fall, or even rise more slowly, the expected return to new investment drops sharply, choking off investment.

Delivering the steady rise in housing supply consistent with sustained slower growth in housing costs demands developers be willing to go forward at lower returns than today’s private markets require. In principle, this could be achieved by shifting more housing development to the public sector or to dedicated nonprofits — a model that has been successful around the world.

But in the short run, such a radical change in the housing-development landscape seems unlikely. A more incremental and immediately achievable step in the same direction is for the public sector to take on a larger role in housing finance.

The required returns on new housing investment are so high because of the riskiness of equity investment in housing, the large share of equity in the overall financing of most housing development projects, and the reluctance of lenders to offer long-term financing at the construction stage — all problems that a public lender could overcome. The public sector’s long horizons, large balance sheets, ability to internalize externalities, and lack of lenders or profit-seeking shareholders, mean that the public sector is better suited to bear the risks and accept the long horizons that housing finance requires. There is a basic mismatch between a building, which is literally rooted in place, but will generate valuable services and the associated income for decades to come, and modern financial institutions, which are geared to maximize liquidity and short-term returns. The public sector is better suited to being the provider of housing finance.

There are many specific models which public housing finance can take. At the federal level, it would be natural to expand the portfolios of the existing GSEs into construction loans. At the state and local level, a variety of revolving loan funds and similar entities exist in scattered places, and could be copied and adopted more widely.

Our emphasis on financing does not mean that other means of addressing housing affordability are not important. The land-use and building-code reforms stressed by YIMBYs have a positive role to play. More deeply affordable units will also require some mix of direct public subsidies and public ownership.

We do not claim that addressing the financing side of the housing problem is, alone, sufficient. But we do claim that it is necessary. Without some form of public financing, building our way to broad affordability is unlikely to succeed.

Authors

Mike Fellman is an economist and real estate investor based in Bayamon, Puerto Rico. He previously worked in housing finance at Freddie Mac. He writes on real estate economics on Substack under the publication name Housing Hell.

J.W. Mason is associate professor of economics at John Jay College of the City University of New York, and a senior fellow at the Groundwork Collaborative.

Acknowledgements

The authors thank Emily DiVito, Alex Jacquez, Cameron Murray, Kitty Richards, Jacob Udell, and Paul Williams for their insights and feedback. Nia Law and Noah Ball-Burack provided research support. Tyler Evans provided graphic design. Siddhartha Mahanta and Jan Boutte provided editorial support.

Appendix

To better demonstrate the inherent financial challenges facing development, we will now go through a hypothetical example. We will focus on redevelopment — or, sites with existing structures which are torn down and replaced with new ones — as this can help elucidate the potential challenges to develop more housing after a policy change such as abolishing single-family zoning. Because most neighborhoods currently zoned for single-family homes that may be primed for higher-density development lack greenfield sites, potential development can be constrained and site acquisition costs higher.

Townhomes replace a single family home

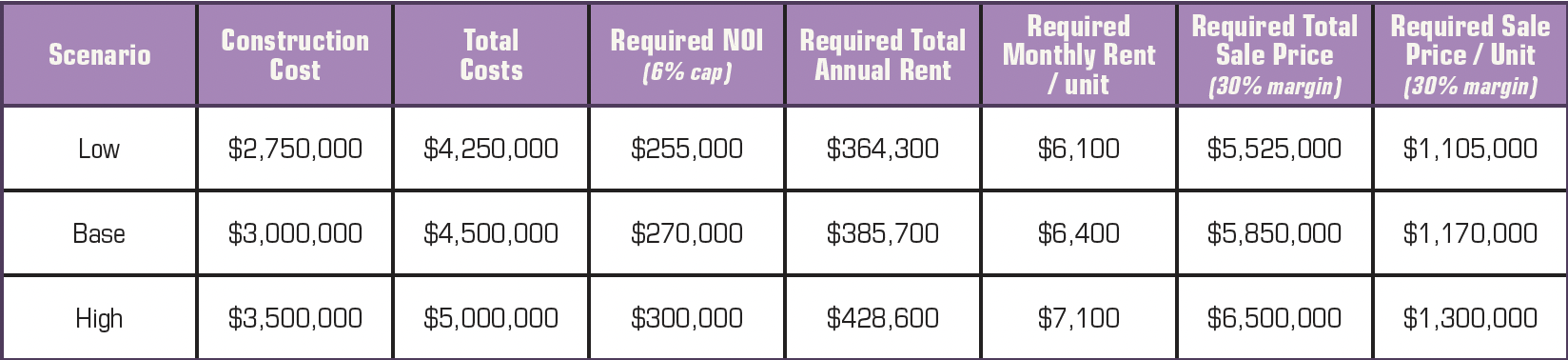

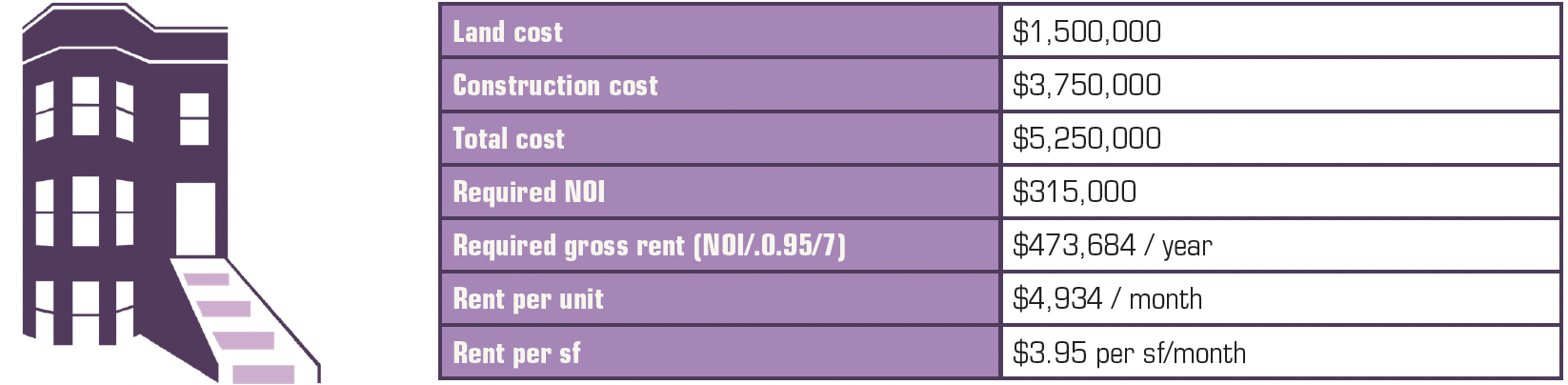

Let’s consider the redevelopment math of a project that acquires a single-family home in an expensive neighborhood, demolishes it, and replaces it with a five-unit townhome development. We envision this project occurring in an area like northwest Washington, D.C., where most homes sell for at least $1.5 million. This is the kind of small infill project that many advocates insist will lead to affordability.

Let’s lay out some brief numbers for this project, either as for-sale townhomes or rentals. Here, we assume a required 6% going-in cap rate if used as rentals or a 30% profit margin if sold off as townhomes. We’ll assume 30% of rent goes to pay operating expenses. Let’s assume each townhome is 2,500 square feet.

Each row represents different baselines for construction costs, based on a $275- to $350-per- square-foot building cost in D.C. Here, required rents to the 6% cap rate target are very high. Let’s see if we can address this higher density.

Now, let’s try reducing the square footage per unit in the townhome development but increase the number of units. Total living space remains 10,000 square feet, but, now, there are eight 1,250-square-foot units. This will likely slightly bump up building costs. We will assume $375 per square foot. Again, we assume 30% of rent goes to expenses, and a 5% vacancy rate.

Here, rents are lower because of lower square footage, but this project is less favorable than the below 10-unit apartment building because total development costs per unit are higher, which occurs because land costs are spread over fewer units.

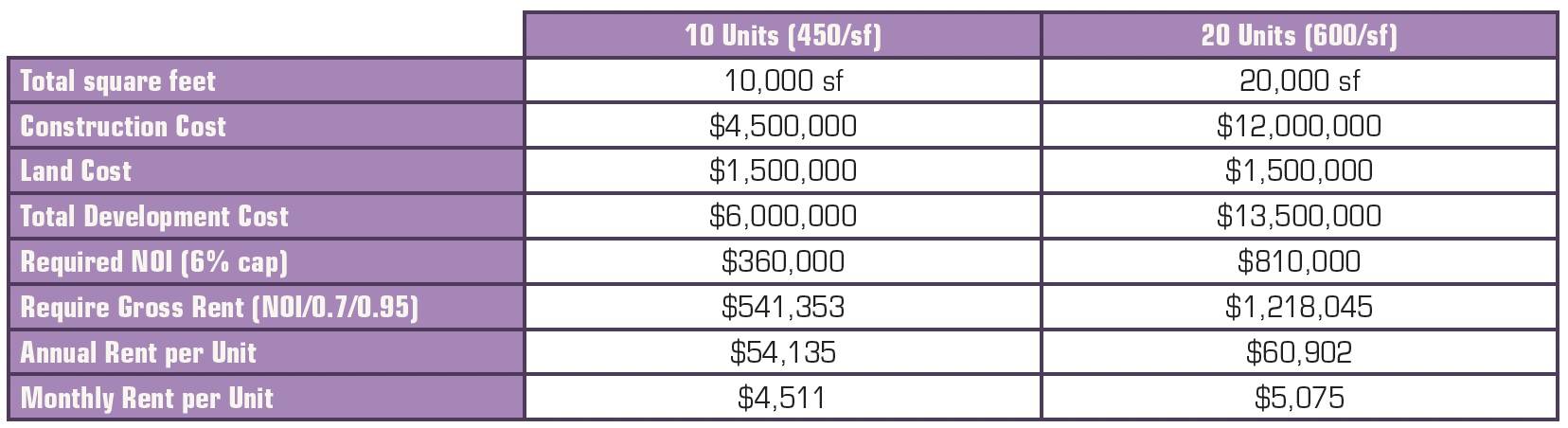

10- and 20-unit buildings replace a single-family home

If we keep site costs fixed at $1.5 million, higher density could potentially lower required rents to hit our 6% cap rate target. However, there are key caveats.

First, since construction costs rise per square foot for much denser projects, rents can only be reduced if square footage per unit falls. Where consumers are willing to make the trade off of less living space in exchange for better location, usually signaled by high land prices, density can be viable.

Let’s compare two potential higher-density projects on the same $1.5-million site. Here, we reduce unit sizes to 1,000 square feet, and assume that to build a 10-unit structure costs $450 per square foot and the 20-unit structure costs $600 per square foot. We keep our assumption of 30% of rent going to cover operating expenses, and add a 5% vacancy rate assumption.

Here, the diseconomies of scale to higher-density building actually require higher rents for the much denser 20-unit project. In the end, under our set of assumptions developers may opt for a midrise 10-unit structure if permitted. However, important caveats must be addressed. Rather than achieving modestly cheaper per unit rents, total living space must be drastically reduced.

Merely upzoning may or may not result in higher levels of density. It depends on where the optimal level of density lies, which is largely a function of market rents per square foot, site-acquisition costs, and construction costs for various construction modes. Many single-family-zoned sites do not support higher levels of density. Or, when they do, they support only a modest increase in density. Here, a midrise, 10-unit building may pencil, with the caveat that market rents may still not support new building.

Endnotes

[1] US Census Bureau, “Nearly Half of Renter Households Are Cost-Burdened, Proportions Differ by Race,” Census.gov, September 12, 2024, https://www.census.gov/newsroom/press-releases/2024/renter-households-cost-burdened-race.html.

[2] Peter J. Mateyka and Jayne Yoo, Share of Income Needed to Pay Rent Increased the Most for Low-Income Households From 2019 to 2021 (U.S. Census Bureau, 2023), https://www.census.gov/library/stories/2023/03/low-income-renters-spent-larger-share-of-income-on-rent.html.

[3] “America’s Rental Housing 2022,” Joint Center for Housing Studies of Harvard University, n.d., 1–44, https://www.jchs.harvard.edu/sites/default/files/reports/files/Harvard_JCHS_Americas_Rental_Housing_2022.pdf; Julia Carpenter, “First-Time Home Buyers Are Older Than Ever,” Real Estate, The New York Times, November 6, 2025, https://www.nytimes.com/2025/11/06/realestate/first-time-home-buyers.html;

Katherine Schaeffer, “Key Facts about Housing Affordability in the U.S.,” Pew Research Center, March 23, 2022, https://www.pewresearch.org/short-reads/2022/03/23/key-facts-about-housing-affordability-in-the-u-s/.

[4] “Housing Activism,” Museum of The City of New York, accessed December 7, 2025, https://www.mcny.org/exhibition/housing-activism; Justin Fox, “New York’s Latest Tenant Revolt Is Centuries in the Making,” Opinion, Bloomberg, July 9, 2019, https://www.bloomberg.com/opinion/articles/2019-07-09/rent-control-in-new-york-is-nothing-new.

[5] Stephen J. Redding, “Suburbanization in the USA, 1970–2010,” Economica 89, no. S1 (2022): S110–36, https://doi.org/10.1111/ecca.12387; U.S. Census Bureau and U.S. Department of Housing and Urban Development, “New Privately-Owned Housing Units Started: Total Units,” HOUST, FRED, September 17, 2025, https://fred.stlouisfed.org/series/HOUST.

[6] Joe Radosevich and Doug Turner, “Americans Recognize Housing Affordability Crisis, Support New Policies To Fix the Market and Build More Homes,” Center for American Progress, October 9, 2024, https://www.americanprogress.org/article/americans-recognize-housing-affordability-crisis-support-new-policies-to-fix-the-market-and-build-more-homes/.

[7] U.S. Census Bureau, “Figure 7: Annual Homeownership Rates for the United States by Age of Householder: 1982-2024,” U.S. Census Bureau, March 18, 2025, https://www.census.gov/housing/hvs/data/charts/fig07.pdf.

[8] S&P Dow Jones Indices LLC, “S&P Cotality Case-Shiller U.S. National Home Price Index,” CSUSHPINSA, FRED, November 25, 2025, https://fred.stlouisfed.org/graph/?g=1MG7y; U.S. Bureau of Labor Statistics, “Consumer Price Index for All Urban Consumers: Rent of Primary Residence in U.S. City Average,” CUUR0000SEHA, FRED, October 24, 2025, https://fred.stlouisfed.org/series/CUUR0000SEHA; U.S. Bureau of Labor Statistics, “Average Hourly Earnings of Production and Nonsupervisory Employees, Total Private,” AHETPI, FRED, November 20, 2025, https://fred.stlouisfed.org/series/AHETPI.

[9] U.S. Bureau of Labor Statistics, “Consumer Price Index for All Urban Consumers: All Items in U.S. City Average,” CPIAUCSL, FRED, October 24, 2025, https://fred.stlouisfed.org/series/CPIAUCSL.

[10] “Homeownership Rate in the United States,” RHORUSQ156N, FRED, July 28, 2025, https://fred.stlouisfed.org/series/RHORUSQ156N.

[11] Matthew Yglesias, “Housing Policy Isn’t That Complicated,” Slow Boring, October 2, 2024, https://www.slowboring.com/p/housing-policy-isnt-that-complicated; Matthew Yglesias, “Inclusionary Zoning Is a Tax on Housing,” Boring, July 14, 2025, https://www.slowboring.com/p/inclusionary-zoning-is-a-tax-on-new.

[12] Edward Glaeser and Joseph Gyourko, “The Economic Implications of Housing Supply,” Journal of Economic Perspectives 32, no. 1 (2018): 3–30, https://doi.org/10.1257/jep.32.1.3; Edward L Glaeser and Joseph Gyourko, “The Impact of Building Restrictions on Housing Affordability,” Federal Reserve Bank of New York Economic Policy Review, June 2003, 21–29; Joseph Gyourko and Jacob Krimmel, “The Impact of Local Residential Land Use Restrictions on Land Values Across and Within Single Family Housing Markets,” Working Paper 28993, National Bureau of Economic Research, July 2021, https://doi.org/10.3386/w28993.

[13] Of course, Thanos’ canonical philosophical orientation is straightforwardly Malthusian — he is quintessentially a NIMBY.

[14] John R. Graham, “Presidential Address: Corporate Finance and Reality,” The Journal of Finance 77, no. 4 (2022): 1975–2049, https://doi.org/10.1111/jofi.13161; Niels Joachim Gormsen and Kilian Huber, “Corporate Discount Rates,” American Economic Review 115, no. 6 (2025): 2001–49, https://doi.org/10.1257/aer.20231246.

[15] “Builder 100 Listings Archive,” Builder Magazine, accessed December 7, 2025, https://www.builderonline.com/builder-100-listing/; There are some exceptions. In Singapore, over 70% of the housing stock was built by the government Housing and Development Board. Interestingly, while housing development in Singapore is mostly public, there is little public housing; Singapore’s 90% homeownership rate is among the highest in the world. In the Netherlands, close to a third of the population lives in social housing which is built, maintained and operated by independent, non-profit housing associations called “woningcorporaties.”

[16] Or, rent minus expenses excluding financing costs, divided by the value of the property. Less frequently, cap rate is called “rental yield.”

[17] Suppose that cap rates in a given area are 6%, and a certain property in said area generates $1,000 a month net of expenses. We can infer its value by multiplying $1,000 by 12 months and dividing by 0.06 to get $216,666.

[18] David Garcia, Making It Pencil: The Math Behind Housing Development (Terner Center for Housing Innovation, 2019), https://ternercenter.berkeley.edu/wp-content/uploads/pdfs/Making_It_Pencil_The_Math_Behind_Housing_Development.pdf.

[19] These numbers are illustrative, but they would not be unusual for a real-world project. In practice, interest rates vary substantially over the business cycle. The returns required by equity investors — while not directly observable — are probably more stable.

[20] 0.4 x 20% + 0.4 x 5% + 0.2 x 15% = 13%.

[21] Typically, projects are refinanced or sold immediately upon completion and leasing out to exit costly construction loans. They are sold again in five years to realize capital gains.

[22]Jonas Vogt, “Housing vs. Stocks — a Simulation Based Comparison of Resulting Real Wealth Distributions,” SSRN Scholarly Paper 4906913 (Social Science Research Network, September 29, 2025), https://papers.ssrn.com/abstract=4906913.

[23] Theresa Kuchler et al., “Housing Market Expectations | NBER,” NBER Working Papers, no. 29909 (April 2022), https://doi.org/10.3386/w29909.

[24] Andreas Mense, Secondary Housing Supply, Working paper, FAU Discussion Papers in Economics (IAB Nuremberg & London School of Economics, 2023), 1–59, https://andreas-mense.de/wp-content/uploads/2023/01/SecondaryHousingSupply.pd; Brian J. Asquith et al., “Local Effects of Large New Apartment Buildings in Low-Income Areas,” The Review of Economics and Statistics 105, no. 2 (2023): 359–75, https://doi.org/10.1162/rest_a_01055; Carlos Garriga et al., “Investors in Housing Markets: Comparing Two Booms,” SSRN Electronic Journal, ahead of print, 2024, https://doi.org/10.2139/ssrn.4687727; Xiaodi Li, “Do New Housing Units in Your Backyard Raise Your Rents?,” Journal of Economic Geography 22, no. 6 (2021): Pages 1309-1352, https://doi.org/10.1093/jeg/lbab034; Yelena Maleyev, “Housing starts fall sharply,” KPMG, June 18, 2025, https://kpmg.com/us/en/articles/2025/may-2025-housing-starts.html;

[25] In the next section, we will examine why rent growth is required to achieve adequate returns to attract private investors.

[26] Tim Henderson, “The Number of New Apartments Is at a 50-Year High, but States Expect a Slowdown,” Stateline, May 1, 2025, https://stateline.org/2025/05/01/the-number-of-new-apartments-is-at-a-50-year-high-but-states-expect-a-slowdown/.

[27] Leslie Shaver, “Apartment Starts Continue to Drop,” Multifamily Drive, May 22, 2024, https://www.multifamilydive.com/news/apartment-starts-condo-construction-build-to-rent/716852/.

[28] Board of Governors of the Federal Reserve System and Freddie Mac, “FRED Graph: Federal Funds Effective Rate and 30-Year Fixed Rate Mortgage Average in the United States,” FEDFUNDS. MORTGAGE30US, FRED, n.d., https://fred.stlouisfed.org/graph/?g=1MG94.

[29] For example, a typical real estate deal might offer a 6% cap rate with 4% underwritten rent growth. On an unleveraged basis, this deal would offer a 10% total return per year, which would fail to clear hurdle rates given the risk and illiquidity of real estate.

[30] Edward E. Leamer, “Housing IS the Business Cycle,” Working Paper 13428, Working Paper Series (National Bureau of Economic Research, September 2007), https://doi.org/10.3386/w13428.

[31] Jung Hyun Choi et al., High Rents Are Posing Financial Challenges for Renters at All Income Levels, Urban Wire (Urban Institute, 2024), https://www.urban.org/urban-wire/high-rents-are-posing-financial-challenges-renters-all-income-levels.

[32] Single-Family Rental Investment Trends Repor, Single-Family Rental Investment Trends Report (Arbor Reality Trust, 2024), https://arbor.com/wp-content/uploads/2024/09/Arbor_Single_Family_Invest_Rental_Report_2024-Q3_VF.pdf; Xander Snyder, “Have Multifamily Cap Rates Peaked?,” First American, August 23, 2024, https://blog.firstam.com/cre-insights/have-multifamily-cap-rates-peaked.

[33] Of particular note to policymakers, in many markets throughout the U.S., replacement costs to market value of existing rental housing can also have a big impact on starts. Investors looking to gain exposure to the real estate market in any metro have the option of buying an existing property or building from the ground up. When the costs to do the latter substantially exceed the costs to buy existing buildings, it makes little sense to build from the ground up. Furthermore, since building values are simply a function of net rental income, in markets with lots of “naturally affordable housing” (and thus low building values), rents usually need to rise substantially to induce building activity. In other words, affordability can substantially erode before any new private building becomes viable. Advocates for more privately financed building to address affordability must contend with the fact that in many markets, affordability would need to substantially decline before private investors would consider building.

[34] Jonathan Jones, American Cities With the Highest Rental Vacancy Rates [2024 Edition], American Cities With the Highest Rental Vacancy Rate (Construction Coverage, 2025), https://constructioncoverage.com/research/cities-with-the-highest-rental-vacancy-rates.

[35] Jordan Berger, “Multifamily Demand Booms Amid Construction Pullback,” CRE Daily, December 6, 2025, https://www.credaily.com/briefs/multifamily-demand-booms-amid-construction-pullback/.

[36] “The Rise of the YIMBYs: A National Pro-Housing Movement,” California YIMBY, April 2, 2021, https://cayimby.org/blog/the-rise-of-the-yimbys-a-national-pro-housing-movement/.

[37] “AB 835 — Build A Wider Variety of Homes,” California YIMBY, n.d., accessed December 7, 2025, https://cayimby.org/legislation/ab-835/; Emily Jacobson and Spencer Richard, “Elements of Zoning,” California YIMBY, n.d., accessed December 7, 2025, https://cayimby.org/map/elements-of-zoning/.

[38] Moses Gates et al., Averting Crisis: Zoning for the Coming Climate Challenge (RPA, 2025), https://rpa.org/work/reports/averting-crisis.

[39] Thomas DiNapoli and Rahul Jain, Housing Production in New York City (Office of the New York State Comptroller), https://www.osc.ny.gov/files/reports/pdf/report-24-2025.pdf.

[40] Tushar Kansal and Alex Horowitz, “Chicago and Washington, D.C., Among Cities Well Suited for Office-to-Co-Living Conversions,” Pew, April 28, 2025, https://pewtrsts.org/447ScnD; Yonah Freemark, “Upzoning Chicago: Impacts of a Zoning Reform on Property Values and Housing Construction,” Urban Affairs Review 56, no. 3 (2020): 758–89, https://doi.org/10.1177/1078087418824672.

[41] Seab Campion, “Why It Costs So Much To Build in New York City,” Vital City, September 17, 2025, https://www.vitalcitynyc.org/articles/why-it-costs-so-much-to-build-in-new-york-city.

[42] Garcia, Making It Pencil: The Math Behind Housing Development, https://ternercenter.berkeley.edu/wp-content/uploads/pdfs/Making_It_Pencil_The_Math_Behind_Housing_Development.pdf; Will Parker, “Apartment Construction Is Slowing, and Investors Are Betting on Higher Rents,” Real Estate, Wall Street Journal, September 2, 2024, https://www.wsj.com/real-estate/apartment-construction-is-slowing-and-investors-are-betting-on-higher-rents-56bceeb3.

[43] Yonah Freemark, “Upzoning Chicago: Impacts of a Zoning Reform on Property Values and Housing Construction,” Urban Affairs Review 56, no. 3 (2020): 758–89, https://doi.org/10.1177/1078087418824672.

[44] Marcel Negret et al., Homes on Track: Building Thriving Communities Around Transit, (Regional Planning Association, 2024); Sogand Karbalaieali, “To Get the Metro We Deserve, Transform Parking into Housing,” Greater Greater Washington, accessed December 7, 2025, https://ggwash.org/view/91237/to-get-the-metro-we-deserve-transform-parking-into-housing; TRANSIT-ORIENTED DEVELOPMENT, Quarterly Status Report (SoundTransit, 2024), https://www.soundtransit.org/sites/default/files/documents/Transit-oriented%20Development%20Quarterly%20Report%20-%20Q4%202024.pdf/

[45] Andjela Padejski and Amy Qin, “Chicago Rents Are Climbing Fast. For Many, There’s Nowhere Left to Go,” WBEZ Chicago, February 26, 2025, https://www.wbez.org/interactive/chicago-rents-climbing-fast-housing-crisis; Michaelle Bond, “Philly Is One of the Least Affordable Major Metros for Its Renters,” Housing, The Philadelphia Inquirer, January 27, 2025, https://www.inquirer.com/real-estate/housing/philadelphia-renters-real-estate-afford-redfin-20250127.html; Winnie Hu and Stefanos Chen, “It Was a Haven for New York Families. Now They Can’t Afford to Stay.,” New York, The New York Times, December 19, 2024, https://www.nytimes.com/2024/12/19/nyregion/washington-heights-nyc-cost-rent.html.

[46] Sanford Ikeda, “How Land-Use Regulation Undermines Affordable Housing,” SSRN Scholarly Paper 3211656 (Social Science Research Network, November 4, 2015), https://doi.org/10.2139/ssrn.3211656; Yonah Freemark et al., Unifying Upzoning with Affordable Housing Production Strategies: Advancing Access to Housing in Washington State (Urban Institute, 2023), https://www.urban.org/research/publication/unifying-upzoning-affordable-housing-production-strategies-report.

[47] “Understanding Building Codes,” NIST, June 16, 2022, https://www.nist.gov/buildings-construction/understanding-building-codes.

[48] Galt, Cal., Municipal Code § 18.48 (Code Publishing 2024), https://www.codepublishing.com/CA/Galt/html/Galt18/Galt1848.html.