Taking on the Annoyance Economy

We call it the “Annoyance Economy” — what we pay in time, fees, and irritation to navigate our daily lives — and it costs Americans at least $165 billion a year.

Read the full report.Hours spent on hold with customer service or lost in convoluted insurance paperwork; the relentless ping of spam calls or political messages warning of doom unless we donate; the steady creep of extra fees and surprise surcharges on everyday transactions. We call it the “Annoyance Economy” — what we pay in time, fees, and irritation to navigate our daily lives.

It’s become a defining feature of modern life: the steady grind of small hassles that eat away at our time, patience, and wallets. Everyday interactions that should be simple too often turn into fraught ordeals, leaving people feeling overwhelmed, ignored, or jerked around.

We call it the “Annoyance Economy” — what we pay in time, fees, and irritation to navigate our daily lives. These costs show up in many forms: hours spent on hold with customer service or lost in convoluted insurance paperwork; the relentless ping of spam calls or political messages warning of doom unless we donate; the steady creep of extra fees and surprise surcharges on everyday transactions. Each year, the Annoyance Economy costs American families at least $165 billion in wasted time and lost money—an amount greater than the GDP of 14 U.S. states—according to our calculations.*

One of us recently endured an especially maddening exchange with an airline after a flight cancellation due to bad weather. At the airport, an agent promised an automatic refund — no further action required. Days passed. Nothing. The app insisted on a phone call to resolve the issue. The call line warned of a “more than two hour” wait. It was 9 p.m. I gave up.

The next day, I tried again, repeating “request refund” to the AI phone agent three times before it appeared to give up on me: “I appear to be having trouble,” it told me, before hanging up. Finally, I turned to the chat function. After ten minutes of scripted back-and forth, I was assured the refund was on its way. It wasn’t. I returned to the chat days later, repeated the same information — first to a chatbot, then a human — and, after another 22 minutes, the refund came through. What should have been a one-click task ate up an hour of my life.

By all accounts, the Annoyance Economy has gotten worse. Over the past two decades, time spent on the phone with customer service is up 60%1. Text messaging, once reserved for conversation with friends and family, now resembles our email spam folders, dominated by unsolicited offers from companies, politicians, and fraudsters. Surprise fees have spread from the travel and banking sectors to everything from concert tickets to food on DoorDash.

Over the past two decades, time spent on the phone with customer service is up 60%.

While seemingly minor, these little annoyances add up. A 2019 survey found that one in four respondents delayed or chose to forego health care due to an administrative task, like scheduling appointments, obtaining information, or resolving premium problems.2 Excessive fees on rental applications can trap people in place. A single mother hoping to move closer to a better job and school might need to apply to a half-dozen apartments — but at $50 or $60 per application, the cost of even trying becomes prohibitive. Spam calls, dismissed as a minor nuisance, exact a real toll. In 2023, Americans lost billions of dollars to phone scams, many of them targeting older adults.3

Some of these annoyances may be unintended — the result of clunky technology, legacy paperwork requirements, and outdated regulations. But many forms of annoyance are more deliberate — cynical attempts to slow consumers down, wear them out, or quietly extract value. Simply put: Companies make it easy for us to do things that they want, but conspicuously difficult to do things that we want, but are not in their interest.

Take the click-to-sign-up, call-to-cancel phenomenon. A study of the newspaper industry found that while every single newspaper allowed online signup, less than half allowed consumers to click to cancel, instead requiring them to call during business hours and sit through wait music and promo offers before canceling.4 Or consider health insurance: Some plans still require out-of-network claims to be submitted by mail, forcing patients to print forms and locate a stamp just to request a reimbursement they’re owed.5 Or air travel: Booking a flight is effortless but getting help when that flight is delayed or when your luggage goes missing can mean hours on hold.

Government interactions, too, are weighed down with annoyances, as anyone renewing their driver’s license at the state DMV or attempting to open a small business can attest.6 Rigid rules and outdated contracting and technology make it hard for agencies to test and improve access to programs and services.

Sometimes these processes are intentionally painful. For years, conservative politicians have thrown obstacles into program requirements to deter eligible Americans from receiving the health care, unemployment, and food benefits they need. In the latest example, the recently passed Republican budget law introduced an avalanche of new paperwork that individuals and families will need to regularly complete to receive health care and nutrition assistance.7 Many will be overwhelmed by the paperwork and will lose their benefits as a result.

We call it the “Annoyance Economy” — what we pay in time, fees, and irritation to navigate our daily lives — and it costs Americans at least $165 billion a year.

Read the full report.Virtually everyone hates the Annoyance Economy. So why does it persist? One reason is that many companies profit from it — and fight to protect it. The airline industry spent millions of dollars opposing a new rule that would have entitled passengers to cash refunds if their flights were significantly delayed (the Trump administration announced in September 2025 it was scrapping the rule).8 Similarly, telecom industry groups sued to block the Federal Trade Commission’s (FTC) proposed “click-to-cancel” rule, which would have required companies to make canceling a subscription as easy as signing up. It’s easy to see why they resisted: One study found that making cancellation more difficult can boost corporate revenues by 14% to over 200%, depending on the product.9

Making cancellation more difficult can boost corporate revenues more than 200%.

Another reason is that policymakers tend to treat annoyances as a second-tier issue, overshadowed by what they see as more urgent economic concerns. To be fair, much of the day-to-day strain on quality-of-life stems from deeper structural problems: the high cost of essential goods and decades of stagnant middle-class wage growth. After all, life is undeniably harder when you’re spending more than $1,000 a month on childcare or enduring hour-long commutes because housing near work is out of reach.10, 11 Congress should take on these big challenges with the ambition and urgency that they demand. But too often, leaders overlook the smaller pain points that add up to what feels like death by a thousand cuts. These issues rarely make it into campaign platforms or become budget priorities, leaving consumers stuck with problems that feel trivial to policymakers but loom large in their actual lives.

Making cancellation more difficult can boost corporate revenues more than 200%. However, for policymakers and politicians who are listening, the Annoyance Economy presents an opportunity: Americans want their political leaders to fix this mess. A 2024 YouGov poll gauged public support of 30 different proposed federal policies, from voting access to lower taxes to expanded financial literacy.12 The most popular? More restrictions on robocalls. A separate survey found that a whopping 77% of likely voters, including 72% of Republicans, supported bans on hidden or extra fees.13

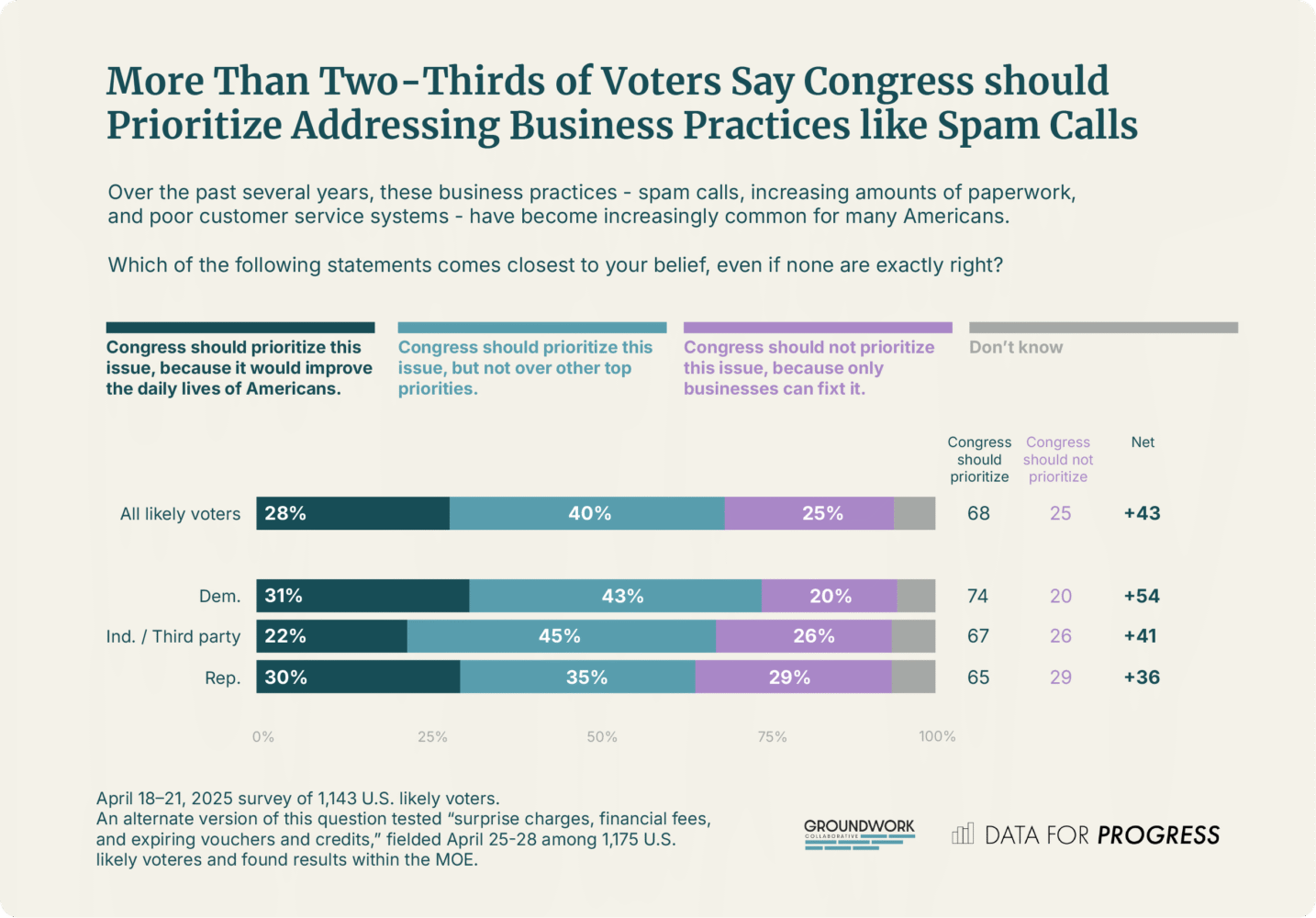

Perhaps most eye-opening is that many Americans put eliminating these pain points at the top of their wish list. In a polarized nation where few policies garner widespread support, new polling from Data for Progress found that more than two-thirds of Americans say it should be a priority for Congress to address these seemingly small-bore frustrations.14

While the current president has shown little interest in standing up for consumers, policymakers from city hall to the halls of Congress can. What follows is the start of an agenda to address some of the Annoyance Economy’s most irksome features. It treats these irritations not as distractions from serious policymaking but as a core opportunity to deliver meaningful, tangible improvements to Americans’ quality of life. Most of these policies can be accomplished using existing authorities, meaning that progress is possible with or without federal legislation.

At a time when most Americans think that their government doesn’t care about them, an all-hands-on-deck effort to tackle the Annoyance Economy would show voters that their elected representatives “get it” — that their daily frustrations are being heard and taken seriously.15 And it would offer something too often missing in politics today: visible improvements to people’s lives.

In our land of plentiful pain points, there is no greater wellspring of annoyance than our country’s health care system. To purchase or select a new plan, you’ll need to learn new vocabulary — from deductible, coinsurance, and copayment to HMO, PPO, and HDHP — and good luck figuring out whether your doctor will be in-network. Booking appointments or obtaining pre-authorization for a medical procedure? Get ready for phone calls, hold music, missed call-backs, and paperwork. And then there’s billing, with confusing explanation-of-benefit letters, out-of-network charges, and facility fees for telehealth visits.

Indeed, an entire cottage industry of so-called “health care concierge” services — available for a fee, of course — has emerged to spare consumers from the friction and frustration built into nearly every step of the health care experience.16

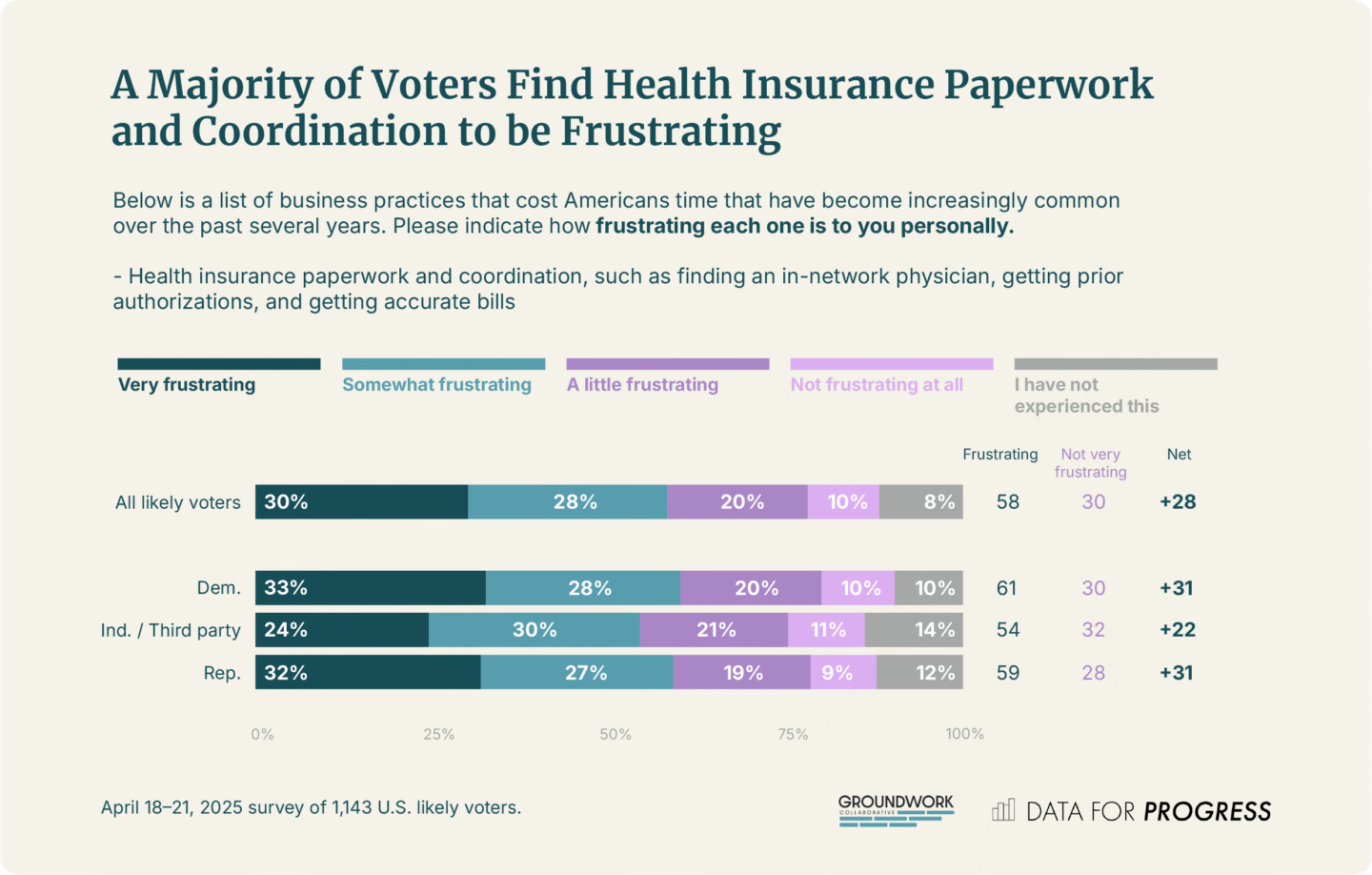

The numbers bear this out. In new polling from Data for Progress, nearly 80% of Americans report at least a little frustration with health insurance paperwork and coordination.17 All told, American workers collectively spend about $21.6-billion-worth of time each year dealing with health care administration, between calls, claims, explanations, and paperwork, according to a recent analysis.18 Polling confirms this: More than one in three Americans report dealing with health insurance headaches more than 20 times per year.

As with many features of the Annoyance Economy, the pain points in the health-care system are too rarely prioritized by policymakers. For decades, Democrats have emphasized the twin goals of expanded coverage and lower costs. With congressional Republicans slashing Medicaid and Affordable Care Act subsidies, policymakers should restore and expand health insurance coverage. And indeed, there is also much work to be done on controlling costs, with prices in the U.S. often twice as high as those in our peer countries.19

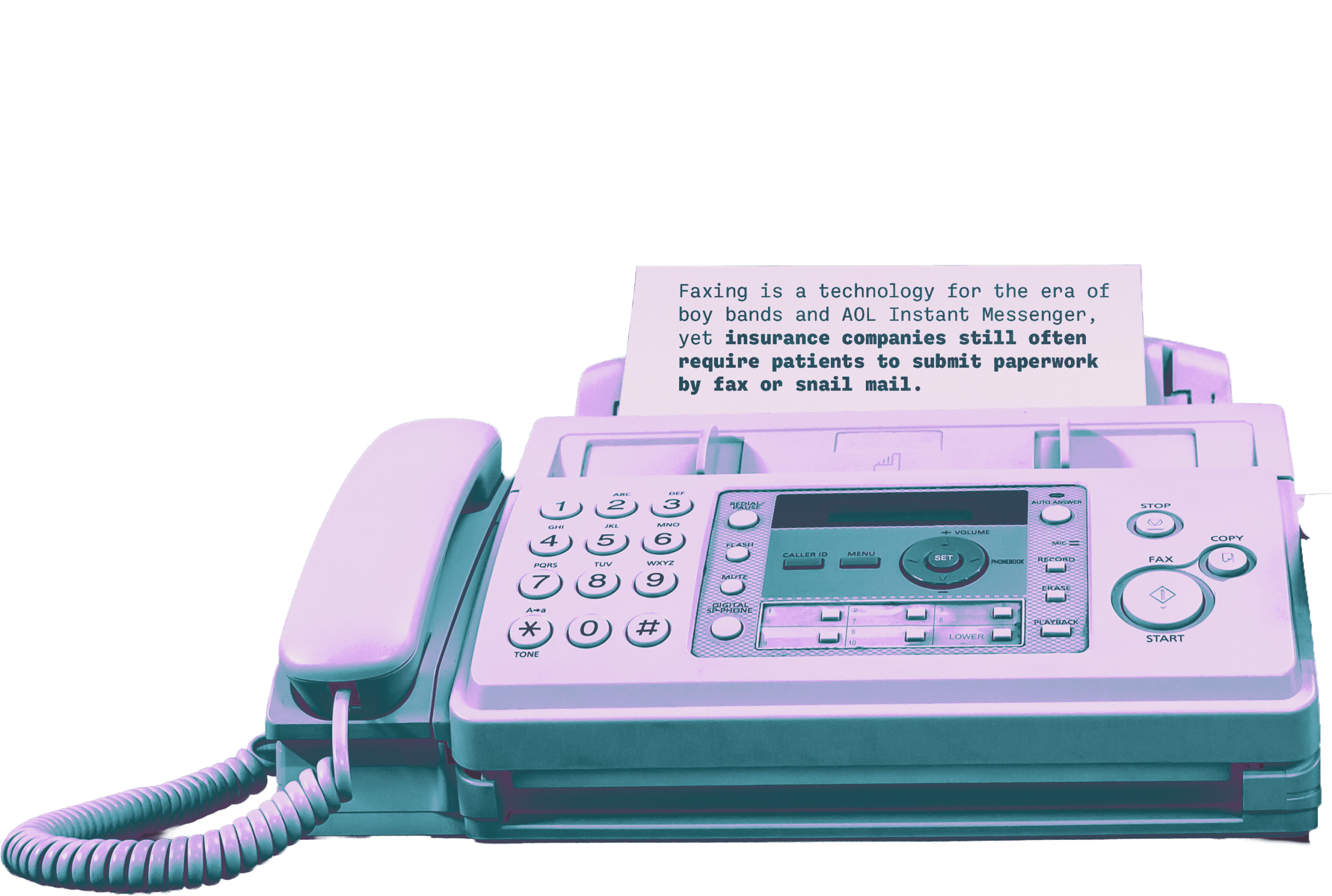

But the issues with the U.S. health care system don’t stop at coverage and costs, and policymakers are missing important opportunities to take on a handful of egregious and particularly annoying practices. For one, insurance companies should make it easy for patients to fill out and submit claims and other forms online. Faxing is a technology for the era of boy bands and AOL Instant Messenger, yet insurance companies still often require patients to submit paperwork by fax or snail mail. Cigna, for example, requires that beneficiaries download, print, and physically mail out-of-network claim forms, along with itemized receipts.20

The use of prior authorization — the requirement by insurance companies to obtain upfront approval for certain drugs, tests, and procedures recommended by your provider — should be appropriate and fast. When shopping for plans, patients should know what they’re signing up for: Insurance companies should publicly disclose average prior authorization denial rates and processing times.

Finally, insurance companies should keep provider directories accurate and up to date, with HHS holding them to account. Outdated provider directories waste people’s time, make it more difficult for them to choose the right plan, and can delay access to medically necessary care.21 A 2024 ProPublica investigation found widespread “ghost” listings — providers shown as in-network who don’t take the insurance or aren’t accepting patients.22

In New York, for example, a blind shopper survey by the Attorney General’s office found 86% of listed mental health providers were unreachable, out-of-network, or closed to new patients.23 Despite clear rules on maintaining updated directories, most states haven’t fined a single insurer for directory errors since 2019.

The list of targets need not end there. Policymakers should create a “Health Care Sludge Unit” charged with monitoring and rooting out needless friction throughout the health care experience — leveraging tools like “blind shopper” experiments, public feedback lines, and direct engagement with industry to surface and fix barriers that waste patients’ time and erode trust. It could also take on the process of selecting health insurance; according to one poll, huge majorities say that shopping for health insurance is worse than getting a cavity filled or sitting in the middle seat on a flight.24

While Congress could end these practices practically overnight, an executive branch that cares about improving consumers’ lives could make meaningful progress using existing authorities. Each year, the federal government purchases health coverage for more than eight million people through the Federal Employees Health Benefits (FEHB) Program, the largest employer-sponsored health plan in the country.25 The Office of Personnel Management (OPM), which oversees the FEHB, already has the authority to embed stronger expectations into the contracts it negotiates. OPM should require plans that want to do business with the federal government to meet a set of requirements to improve the patient experience. They could refuse to do business altogether with plans that don’t make changes across the market, not just FEHB plans. If plans don’t act, either Congress or the Department of Health and Human Services and the Department of Labor could require certain changes through new rulemaking.

States, too, can act. A 2023 Massachusetts regulation requires regular audits of providers’ directory information and mandates that plans provide a phone number that members can call to find an in-network provider.26 And recent legislation in New Jersey mandates that insurers respond to urgent-medication prior authorization requests within 24 hours, down from 15 days.#27 Every state in the nation could be taking similar steps on behalf of consumers.

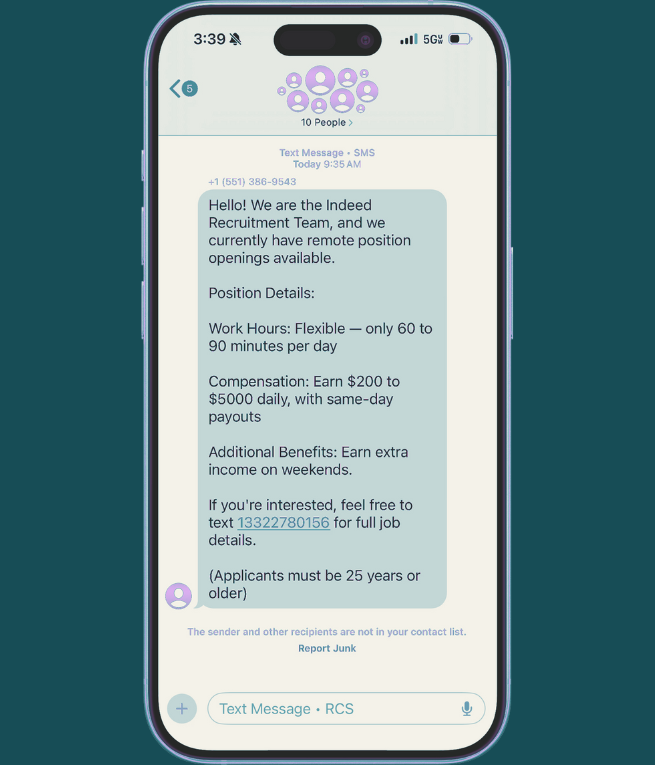

On the day this paragraph was written, one of us received five spam calls, a text from “Victoria” offering a $500-a-day job, and two breathless fundraising messages from political candidates we’ve never supported — or even heard of.

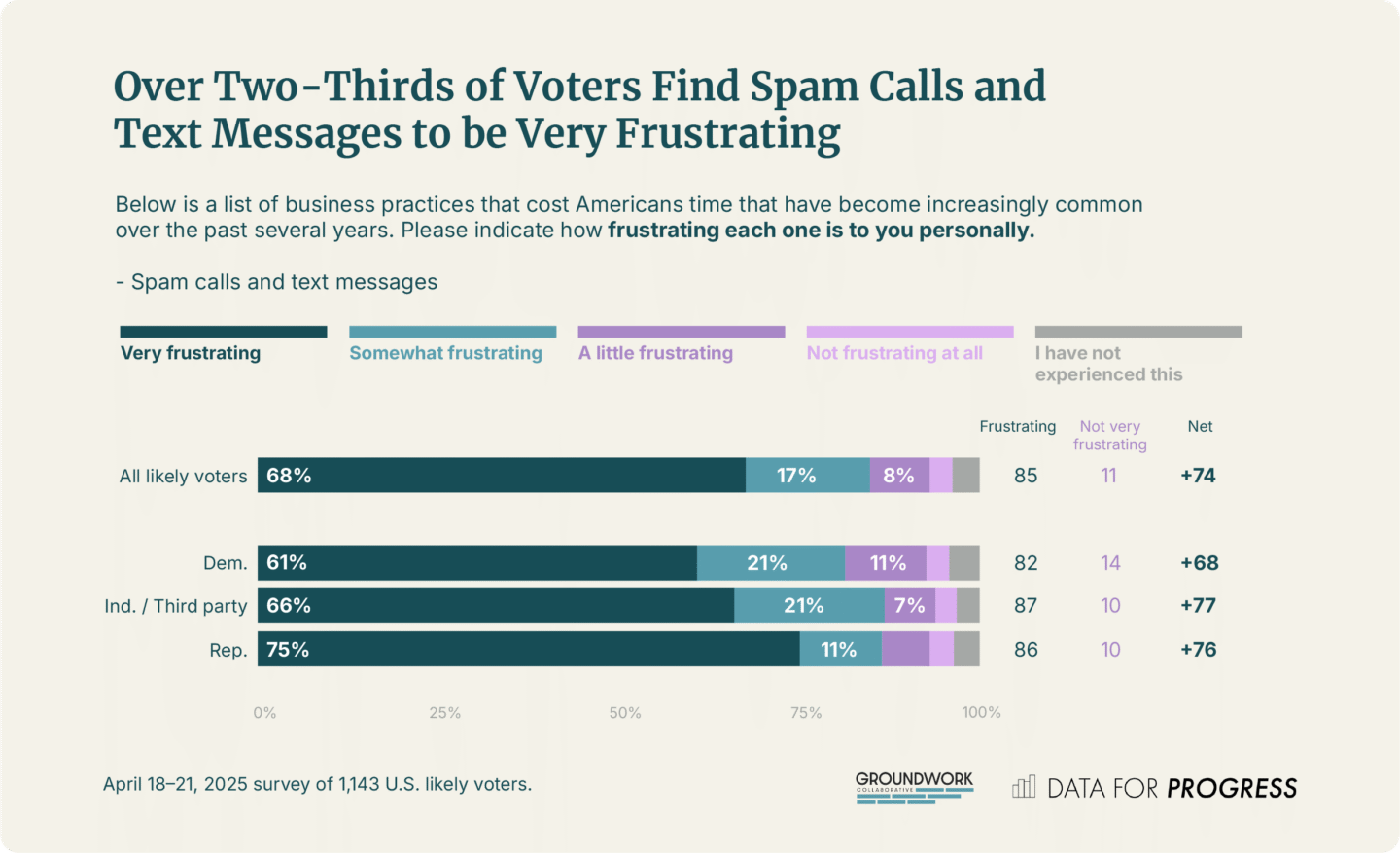

That’s not uncommon. Americans receive nearly four billion scam and illegal marketing calls each month, or more than 130 million a day.28 Spam texts are surging too, with nearly 20 billion messages sent each month over the past year.29

This deluge of digital junk annoys just about everybody. Data for Progress found that virtually all respondents said spam calls and texts were at least “a little frustrating,” and 68% found them “very frustrating”.30 Nearly half said they’d be willing to pay money just to make them stop.

Yet no candidate for federal office runs on a platform of ending spam texts; once elected, few make it a priority. Meaningfully addressing the issue requires sustained coordination across multiple federal agencies and private carriers, the kind of high-engagement, cross-sector effort that doesn’t materialize without political will or public outcry. And in the case of texting, that political will is hard to come by when elected officials themselves rely on it as a cheap and effective way to reach voters.31

Congress could — and should — act to stem the flood of robocalls and spam texts. We can start by modernizing our foundational laws. In Facebook v. Duguid, the Supreme Court narrowed what counts as an “automatic telephone dialing system” under the Telephone Consumer Protection Act (TCPA) — a law meant to protect consumers from unwanted calls and texts — so that it no longer covers many of the newest and most prolific robocalling and texting systems.32 If a platform automatically dials from a stored list of numbers, it’s now exempt from the TCPA’s rules. The result: far more robocall and spam text operations can legally target people without their consent. Congress should update the definition of autodialer to include any callers and texters who automatically contact stored numbers, unless there’s real human involvement in sending each message.

Under current law, entering your phone number on one website can trigger a cascade of calls and texts from companies you’ve never heard of, often without your informed consent. Congress should close the so-called “lead generator loophole,” which allows third-party marketers to collect your contact information and sell it to dozens, sometimes hundreds, of businesses.33

Under the Biden administration, the Federal Communications Commission (FCC) tried to close this loophole, but companies benefiting from the current law sued and won in court.34 Congress can fix this by requiring companies to obtain clear, one-to-one permission before making contact — so that you only hear from the company you explicitly permitted to contact you. These two proposals would significantly reduce the number of unwanted calls and texts interrupting our days.

But we need not wait for Congress to start making progress. The President should issue an executive order (EO) directing or encouraging agencies to leverage all available resources and authorities to end robocalls and spam texts once and for all. EOs help to signal to agencies and the public which issues are priorities and which are not. Yet of the more than 1,000 EOs issued in the past two decades, not one has taken on robocalls and texts.

Such an EO would push agencies to take more forceful action using tools already in their toolkit. One way to crack down on robocalls is to go after the companies that carry them. The FCC should be able to quickly suspend bad actors from the phone network. If a carrier is notified that it’s sending scam calls and doesn’t stop, it would immediately be blocked from routing calls through the U.S. system. Working with the Ohio attorney general, the Biden FCC took some steps in this direction, shutting down auto-warranty scammers who had plagued American consumers for years.35 But we need to do more, more quickly, to give providers a strong incentive to stop illegal traffic before it ever reaches consumers.

Federal and state enforcement agencies need additional resources to go after telecommunications providers that transmit high volumes of illegal calls. Recently, the North Carolina attorney general warned that nearly 200 million illegal calls — ones impersonating Amazon, Apple, the IRS, and the Social Security Administration — could be attributed to a single provider: a voice over IP company called Lingo.36 However, according to the National Consumer Law Center, despite their best efforts to crack down on Lingo and others, “neither the FCC, the FTC, nor the state AGs in all 50 states, have sufficient governmental resources to stop these tens of millions of scam calls from being delivered to U.S. telephone subscribers.”37

Recent reductions to the enforcement agency workforces as a result of President Trump’s Department of Government Efficiency (DOGE) will make matters worse.38 The Department of Justice (DOJ) also needs to prioritize enforcement against bad actors. While the FCC can levy fines for violations, it cannot pursue their collection without the DOJ.39 Of the eight robocalling forfeiture orders referred by the FCC, the DOJ has pursued only two for collection.40

Policymakers should also close the loophole that allows “peer-to-peer” (P2P) texting platforms — often used by political campaigns and causes — to send billions of unsolicited messages. Under federal law, automated texts generally require prior consent, but the Facebook v. Duguid decision created a technicality that P2P platforms exploit to bypass these rules. As Scott Goodstein, who helped pioneer texting for the 2008 Obama campaign, has put it: “Texting an entire voter file of unsuspecting voters is not peer-to-peer communication.”41

Further, the federal government could fight spam texts by creating a text messaging focused Industry Traceback Group (ITG), which would bring together government and phone companies to trace illegal traffic back to the source. An ITG for text messages would work with carriers and text platforms to track down the origin of scam texts and shut them off at the source. This kind of coordinated traceback effort has already proven effective in holding bad actors accountable in the robocall space and could serve as a powerful enforcement and deterrence tool against text-based spam as well.

Terrible customer service has become an increasingly familiar feature of modern life. The research firm Forrester’s CX Index, which measures people’s perceptions of customer service, found that customer experience scores in 2024 were the lowest on record.42 The aptly named Consumer Rage Survey found that 74% of customers reported a product or service problem in the past year, more than double the rate in 1976.43

Many of the customer-service doom loops are the result of affirmative corporate policy. The Consumer Financial Protection Bureau (CFPB) alleged that Comerica Bank adopted a policy known as “Heavy Queue,” whereby they would intentionally drop calls before customers could reach a representative.44 The payments app CashApp was fined for, among other things, providing a fake customer service line that simply directed consumers to a pre-recorded message.45 A journalist from Business Insider recounted a recent experience with her health insurance plan, which seemed intent on preventing her from ever speaking to a live agent, first requiring her to interact with a chatbot and then with an AI agent — neither of which was capable of understanding her problem, though both were adept at wasting her time.46

While not all cases are as egregious, the reality is that for companies today, there’s too little downside to providing bad customer service and too little reward for doing the opposite. Consumers now have more reliable information about what to expect from a dinner reservation or vacation rental than they do when making high-stakes decisions like choosing a health insurance plan or a bank.

Worse, many firms have inoculated themselves against the consequences of bad service by designing systems that make it hard for customers to “shop with their feet” and switch providers. A judge found that SiriusXM forced customers to speak to a live agent and endure as many as five retention offers before being allowed to cancel their subscriptions.47 Until the CFPB intervened in 2023, Toyota Motor Credit routed consumer calls through a hotline where representatives were instructed to keep promoting products until a consumer asked to cancel three times, at which point they were told cancellation was only possible by submitting a written request.48 This dynamic is often exacerbated by increased consolidation across many sectors; consumers know that even if they manage to run the gauntlet of hoops and hurdles to extricate themselves from their unhappy business relationship, there are few options on the other side.

Frustratingly, the Trump administration has made things worse, dropping enforcement actions and withdrawing from settlements with bad actors that would have delivered hundreds of millions of dollars to consumers.49 Policymakers should be pursuing the exact opposite course: cracking down on time-sucking corporate practices and empowering consumers through a functioning market that rewards good customer service.

We can start by making companies pay —literally — for wasting people’s time. Today, legal remedies often overlook the real cost of harder-to-measure harms — like the hours a customer spends navigating deliberately frustrating phone trees or waiting on hold without any prospect of successful resolution.

Unlike lost wages or out-of-pocket expenses, the harm caused by such corporate policies and tactics is rarely factored into how payouts are calculated. Consumer protection agencies like the FTC or CFPB could change this by developing and adopting models for monetary relief that explicitly value consumers’ time.† Or Congress could simply include automatic penalties that pay people for the time they lose when companies waste it.

We can start by making companies pay — literally — for wasting people’s time.

Further, federal agencies can leverage existing tools to make customer service just a little less painful. For example, they could require that companies in regulated industries give customers a clear way out of endless automated phone menus by bringing back the once-common “press zero to speak to a live agent” option. Agencies should also use their authority to collect and disseminate information on key consumer experience metrics, like wait times, refund friction, and success resolving inquiries, in regulated industries. The information can be rolled up into public ratings — think crash test ratings, however, for consumer experience — and used by third parties to create their own recommendation systems in ways that are easy to understand and avoid information overload.

Under Secretary Pete Buttigieg, the Department of Transportation unveiled a customer service dashboard that showed each airline’s policies on things like family seating and refund policies.50 The move not only empowered consumers, it also drove immediate policy change. Before the dashboard launch, none of the 10 largest U.S. airlines guaranteed meals or hotel accommodations when delays were their fault. Today, all 10 guarantee meals, and nine provide hotel stays in those cases. Federal agencies could pursue similar tactics with companies in their purview, like the CFPB with banks, the FCC with telecom providers, and HHS with health-insurance plans. Some consumers may continue to make decisions based on the lowest price, but others will place weight on avoiding annoyances, and the greater transparency will provide market incentives for companies to provide better customer service.

These rules can be strengthened with automatic renewal laws that require notification when plans convert from a free trial to a paid subscription or renewal, and with use-it-or-lose-it provisions that require reminders and auto-pause for inactive users (e.g., pausing payments for a consumer who has not used a streaming service in six months).

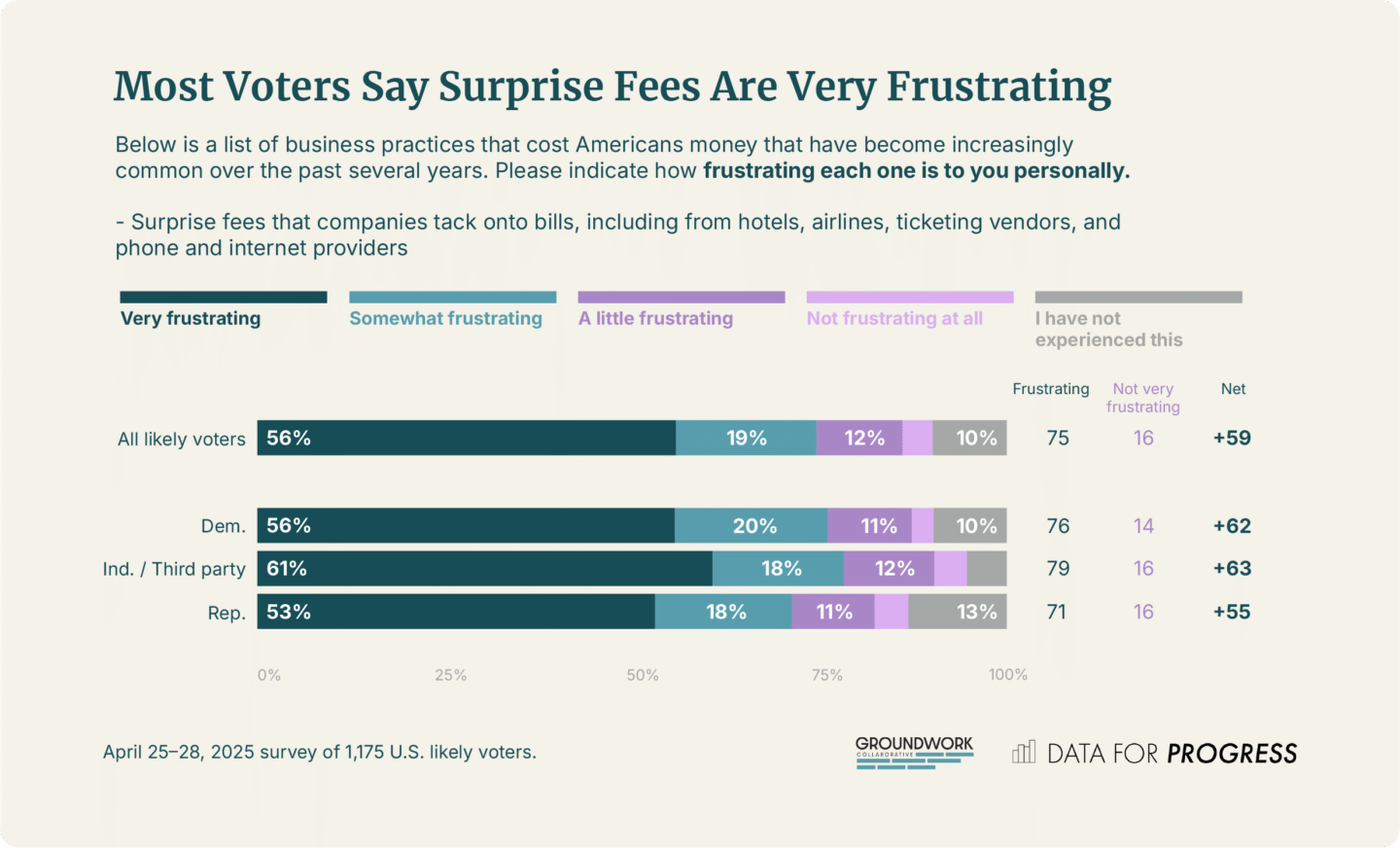

Finally, there’s the scourge of junk fees, those surprise add-ons and surcharges that seem to make their way onto every bill these days. Twenty dollars here, 10 dollars there — they add up. An analysis by the White House Council of Economic Advisers of 10 specific junk fees found that they amount to $90 billion per year, or $650 per household per year on average.51 Even when the costs are small, having junk fees added to your bill is incredibly annoying. Data for Progress found 56% of voters said that surprise fees were “very frustrating” and 87% said they were at least “a little frustrating.”

While seemingly small ball policies like junk fees often get short thrift, the Biden administration went all in. Perhaps the highest profile of these is a landmark FTC rule prohibiting hidden and misleading fees in the live-event ticketing and short-term lodging industries. Instead of inserting surprise service and resort fees at check out — a practice sometimes referred to as “drip pricing” — the rule requires all-in, up-front pricing of hotel rooms and event tickets, allowing consumers to shop around for the best available price.

The CFPB also took action on unfair — and extremely annoying — fees in banking, including cracking down on excessive overdraft fees.52 The overdraft rule, repealed by Trump and congressional Republicans, would have protected Americans from being charged fees of up to $35 for small purchases, like a cup of coffee or a bus ticket, that briefly overdrew their account.53 Biden’s focus on junk fees was overwhelmingly popular, including support from two-thirds of Republicans.54

To build on this progress, the FTC could take rulemaking a step further, rooting out hidden fees in every corner of the economy. Take rental application fees. Prospective renters often spend $50 or more just to apply for an apartment; in a hot rental market in which people often apply to many apartments, this can add up to hundreds of dollars without any guarantee of success.

Background checks shouldn’t be a revenue generator for landlords. Policymakers could, at minimum, cap credit check fees at the actual cost of running the check — typically between $15 and $40 — and allow renters to pay once and use a single, reusable rental application for multiple properties.55

Or consider fees in food delivery apps. At this point, most of us are familiar with the dynamic: you go through the process of crafting the perfect order, only to learn at checkout that the price of your $10 meal has somehow doubled. “All-in” pricing should be the rule, not the exception.

Finally, the FTC could ban, altogether, fees that provide nothing of value — for example, the common practice by rental car companies of charging “extra driver fees.”56 Typically, this amounts to $10 to $15 per day just to add a second authorized driver. These fees have no clear rationale and can add $100 or more to the cost of a family vacation. States are going hard on junk fees and offer a path for others to follow suit. Some states have capped rental application fees at a fixed amount, or the amount it actually costs for the landlord to screen the applicant.57 In New York, state law caps the fee for a second driver to a rental car at $3 a day.58 And beginning in 2025, restaurants and hospitality businesses in Minnesota are banned from adding undisclosed fees like health or wellness surcharges to customer bills.

For most people, the Annoyance Economy isn’t an abstract concept but a daily reality of wasted hours and drained wallets — to the tune of more than $165 billion per year. These hassles are a universal experience, impacting virtually every American and piling onto families already stretched by the high costs of housing, child care, and other necessities.

Our Econ 101 textbooks teach that a central tenet of our economy is competition: businesses strive to offer the best products and services for the best price, and those that succeed are rewarded with more customers and revenue. But somewhere along the way, that relationship has broken down. Market power grew increasingly concentrated in the hands of a few dominant players. Federal oversight weakened and enforcement lagged. Both federal and state policy failed to keep pace with the speed of technological change and innovation. Artificial intelligence is already supercharging the tactics that companies use to extract time and money from consumers.

The consequences of our Annoyance Economy extend beyond wasted time and money: When life is reduced to jumping through an endless series of hoops — just to fix a billing error, secure a refund, or cancel a subscription, it breeds cynicism and disengagement. If the government can remove even a few of those obstacles, we can show the American people that someone is paying attention and begin the long process of rebuilding public trust.

Today, the problems our nation faces feel impossibly big. But for policymakers eager to solve them, we argue that the first step is to think small.

Chad Maisel is a Policy Fellow at Groundwork Collaborative. Maisel was most recently Special Assistant to the President for Housing and Urban Policy at the Domestic Policy Council. He previously served as an economic policy advisor to Senator Cory Booker, including as Deputy Policy Director on his 2020 presidential campaign, and in the Obama administration in the White House, the Office of Management and Budget, and the Department of Agriculture. Maisel’s work focuses on policy solutions to confront economic pain points and ways that corporations and other actors rob people of their time and money.

Neale Mahoney is the Trione Director of the Stanford Institute for Economic Policy Research (SIEPR) and TG Wijaya Professor of Economics at Stanford. He’s a leading scholar with expertise in healthcare, consumer financial, energy, and housing markets, and he regularly advises policymakers in state and federal government on economic policy issues. He served in the National Economic Council in the Biden Administration and worked on healthcare reform in the Obama Administration. He received a PhD in Economics from Stanford and started his career as Professor of Economics at the University of Chicago Booth School of Business.

The authors thank Thuy Minh Le, Sam Levine, Rohit Chopra, Christen Linke Young, Jess Schubel, Margot Saunders, Scott Goodstein, Tara Mikkilineni, Andrés Argüello, Emily DiVito, Liz Pancotti, and Alex Jacquez for their insights and feedback. Siddhartha Mahanta and Jan Boutte provided editorial support and Matt Ingram provided graphic design.

[*] Authors’ calculation based on approximate time spent conducting each activity and average hourly earnings. Calculated using the American Time Use Survey, population data from the Census, wage data from the Federal Reserve Bank of St. Louis, as well as data from TrueCaller, Pfeffer et. al (2020), and the Council of Economic Advisors.

[†] Agencies could publish valuation frameworks that assign monetary weight to consumer time, which would be incorporated into redress and penalty calculations in individual cases. Agencies could also make clear that they will pursue civil penalties against companies that intentionally waste people’s time and pursue maximum revenue under law. Together, these approaches could be a deterrent, as companies would need to determine whether the benefits of their time-wasting tactics outweigh the risk of financial penalty.

[1] U.S. Bureau of Labor Statistics, American Time Use Survey (Washington, DC: U.S. Department of Labor), https://www.bls.gov/tus.

[2] Michael Anne Kyle and Austin B. Frakt. “Patient Administrative Burden in the US Health Care System.” Health Services Research 56, no. 5 (September 8, 2021): 755–65. https:// doi.org/10.1111/1475-6773.13861.

[3] TrueCaller, “America Under Attack: The Shifting Landscape of Spam and Scam Calls in America,” March 2024. https://drive.google.com/file/d/1M0J0wO6YqxDzsOizfal-AH_vI8dsyojb/view.

[4] Giacomo Fraccaroli, Neale Mahoney, and Zahra Thabet. “How Big Is the Subscription Cancellation Problem?” Briefing Book (blog), September 9, 2024. https://www.briefingbook.info/p/how-big-is-the-subscription-cancellation.

[5] United HealthCare Services, Inc., “Medical Claim Form,” 2019. https://member.uhc.com/myuhc/content/dam/myuhc/pdfs/claim-forms/CMS1500ClaimForm010402.pdf.

[6] Zohran Mamdani for NYC. “NYC Is Suffering From Halalflation,” YouTube video, January 13, 2025. https://www.youtube.com/watch?v=QyL4PsmA3u8.

[7] Editorial Board, “The One Big Beautiful Bill Would Tangle Obamacare in Red Tape.” The Washington Post, June 24, 2025. https://www.washingtonpost.com/opinions/2025/06/24/obamacare-aca-reconciliation-bill-uninsured/.

[8] Federal Register. “Airline Passenger Rights; Withdrawal,” November 17, 2025. https://www.federalregister.gov/documents/2025/11/17/2025-20042/airline-passenger-rights-withdrawal.

[9] Liran Einav, Benjamin Klopack, and Neale Mahoney, “Selling Subscriptions,” August 1, 2023. https://doi.org/10.3386/w31547.

[10] Georgia Poyatzis and Gretchen Livingston, “NEW DATA: Childcare Costs Remain an Almost Prohibitive Expense.” DOL Blog (blog), November 19, 2024. https://blog.dol.gov/2024/11/19/new-data-childcare-costs-remain-an-almost-prohibitive-expense.

[11] US Census Bureau, “United States Commuting at a Glance: American Community Survey 1-Year Estimates.” Census.gov, September 22, 2025. https://www.census.gov/topics/employment/commuting/guidance/acs-1yr.html.

[12] YouGov, “YouGov Survey: Policy Support.” Report, May 2024. https://d3nkl3psvxxpe9.cloudfront.net/documents/Policy_Support_May_13.pdf.

[13] Timothy Bresnahan, “Voters Support Initiatives to Lower Drug Costs, Ban Junk Fees, and Strengthen Supply Chains.” Data for Progress, December 12, 2023. https://www.dataforprogress.org/blog/2023/12/12/voters-support-initiatives-to-lower-drug-costs-banjunk-fees-and-strengthen-supply-chains.

[14] Data for Progress, “Business Practices Impacting Americans’ Time: A Survey Analysis,” Report, 2025. https://www.filesforprogress.org/datasets/2025/4/dfp_gwc_frustrating_business_practices.pdf.

[15] Katherine Schaeffer, “More Than 80% of Americans Believe Elected Officials Don’t Care What People Like Them Think.” Pew Research Center, July 9, 2024. https://www.pewresearch.org/short-reads/2024/04/30/more-than-80-of-americans-believe-elected-officials-dont-care-what-people-like-them-think/.

[16] Kara Miller, “Some Patients Are Paying up to $50,000 per Year in Fees for ‘Concierge Medicine.’ Here’s What’s Behind Its Rise.” STAT, November 15, 2024. https://www.statnews.com/2024/11/15/patients-concierge-medicine-primary-care/.

[17] Data for Progress, “Business Practices Impacting Americans’ Time: A Survey Analysis.”

[18] Jeffrey Pfeffer, Dan Witters, Sangeeta Agrawal, and James Harter, “Magnitude and Effects of ‘Sludge’ in Benefits Administration: How Health Insurance Hassles Burden Workers and Cost Employers,” Academy of Management Discoveries, July 31, 2020. https://doi.org/10.5465/amd.2020.0063.

[19] Munira Z. Gunja, Evan D. Gumas, and Reginald D. Williams II, “U.S. Health Care From A Global Perspective, 2022: Accelerating Spending, Worsening Outcomes,” The Commonwealth Fund, January 11, 2023, https://doi.org/10.26099/8ejy-yc74.

[20] “Health Claims and Explanation of Benefits,” Cigna Health Care, n.d. https://www.cigna.com/individuals-families/member-guide/claims-and-eobs.

[21] Neel M. Butala, Kuldeep Jiwani, and Emily M. Bucholz, “Consistency of Physician Data Across Health Insurer Directories,” JAMA 329, no. 10 (March 14, 2023): 841, https://doi.org/10.1001/jama.2023.0296.

[22] Max Blau, “State Regulators Know Health Insurance Directories Are Full of Wrong Information. They’re Doing Little to Fix It,” ProPublica, November 15, 2024. https://www.propublica.org/article/ghost-networks-health-insurance-regulators.

[23] Office of the New York State Attorney General, Inaccurate and Inadequate: Health Plans’ Mental Health Provider Network Directories, December 7, 2023. https://ag.ny.gov/sites/default/files/reports/mental-health-report_0.pdf.

[24] Kathryn Mayer, “People Hate Shopping for Health Insurance.” BenefitsPRO, February 18, 2018. https://www.benefitspro.com/2014/12/02/people-hate-shopping-for-health-insurance.

[25] U.S. Office of Personnel Management, “FEHB Carriers,” n.d. https://www.opm.gov/healthcare-insurance/carriers/fehb/.

[26] Eric Gold, “MA Issues New Insurance Regulation on Provider Directories, Telehealth & Behavioral Health Parity,” December 18, 2023. https://www.manatt.com/insights/newsletters/health-highlights/massachusetts-issues-new-health-insurance-regulati.

[27] Tina Shah and Devika Bhushan, “Other States Should Follow New Jersey’s Lead on Prior Authorization Reform,” STAT, February 1, 2024. https://www.statnews.com/2024/01/25/prior-authorization-reform-new-jersey-washington-federal-law-cms/.

[28] “YouMail Robocall Index: November 2025 Nationwide Robocall Data,” YouMail, n.d. https://www.robocallindex.com/.

[29] U.S. PIRG Education Fund, “Ringing in Our Fears 2024,” December 12, 2024. https://pirg.org/edfund/resources/ringing-in-our-fears-2024/.

[30] Data for Progress, “Business Practices Impacting Americans’ Time: A Survey Analysis.”

[31] Nancy Scola, “Why Are Annoying Political Texts Out of Control?” Washingtonian, February 20, 2025. https://washingtonian.com/2024/10/24/why-are-annoying-political-textsout-of-control/.

[32] Facebook, Inc. v. Duguid et al, 592 U.S. (2021).

[33] Brief for the National Consumer Law Center, Electronic Privacy Information Center, Consumer Federation of America, U.S. PIRG, and Public Knowledge as Amicus Curiae Supporting Respondents, Insurance Marketing Coalition Ltd. v. Federal Communications Commission, No. 24-10277 (11th Cir. July 22, 2024).

[34] Insurance Marketing Coalition Ltd. v. Federal Communications Commission, No. 24-10277 (11th Cir. July 22, 2024).

[35] Irina Ivanova, “FCC Cracks Down on Scam ‘Auto Warranty’ Robocalls.” CBS News, July 22, 2022. https://www.cbsnews.com/news/robocalls-auto-warranty-scam-federal-communictions-commission/.

[36] Tracy Nayer, Special Deputy Attorney General, North Carolina Department of Justice, to Ananth Veluppillai, CEO, Lingo Telecom, LLC, April 9, 2025, https://ncdoj.gov/wp-content/uploads/2025/04/State-AG-Task-Force-2nd-NOTICE-Letter-to-Lingo-Apr-2025.pdf.

[37] National Consumer Law Center, “Letter to JEC,” n.d. https://www.nclc.org/wp-content/uploads/2025/07/Email-to-JEC-6-16-25.pdf.

[38] Brendan Carr, Chairman, Federal Communications Commission, to Steny H. Hoyer, May 7, 2025. https://docs.fcc.gov/public/attachments/DOC-413388A4.pdf.

[39] Jon Brodkin, “FCC Robocall Enforcement Does Little to Stop Illegal Calls, Senate Hears,” Ars Technica, October 24, 2023. https://arstechnica.com/tech-policy/2023/10/many-robocallers-dont-pay-fines-as-fcc-still-lacks-legal-power-to-collect/.

[40] Congress.gov, “S.Hrg. 118-606 — PROTECTING AMERICANS FROM ROBOCALLS.” December 4, 2025. https://www.congress.gov/event/118th-congress/senate-event/LC74133/text.

[41] “An Interview With Scott Goodstein About Political Text Messaging,” Vocal Media, August 11, 2022. https://vocal.media/interview/an-interview-with-scott-goodstein-about-political-text-messaging.

[42] “Forrester Releases 2024 US Customer Experience Index,” Forrester, June 17, 2024. https://www.forrester.com/press-newsroom/forrester-2024-us-customer-experience-index/.

[43] “Historic National Customer Rage Survey,” W. P. Carey School of Business, March 7, 2023. https://news.wpcarey.asu.edu/20230307-historic-national-customer-rage-survey.

[44] Consumer Financial Protection Bureau, “CFPB Sues Comerica Bank for Systematically Failing Disabled and Older Americans,” December 6, 2024. https://www.consumerfinance.gov/about-us/newsroom/cfpb-sues-comerica-bank-for-systematically-failing-disabled-and-older-americans/.

[45] Consumer Financial Protection Bureau, “CFPB Orders Operator of Cash App to Pay $175 Million and Fix Its Failures on Fraud,” January 16, 2025. https://www.consumerfinance.gov/about-us/newsroom/cfpb-orders-operator-of-cash-app-to-pay-175-million-and-fixits-failures-on-fraud/.

[46] Emily Stewart, “The Future of Customer Service Is Here, and It’s Making Customers Miserable,” Business Insider, November 26, 2024. https://www.businessinsider.com/ai-chatbots-customer-service-call-center-annoying-problems-2024-11.

[47] Emma Roth, “Judge Rules SiriusXM’s Annoying Cancellation Process Is Illegal,” The Verge, November 22, 2024. https://www.theverge.com/2024/11/22/24303294/sirius-xm-cancellation-process-illegal-ny-ag.

[48] Consumer Financial Protection Bureau, “CFPB Orders Toyota Motor Credit to Pay $60 Million for Illegal Lending and Credit Reporting Misconduct,” November 20, 2023. https://www.consumerfinance.gov/about-us/newsroom/cfpb-orders-toyota-motor-credit-to-pay-60-million-for-illegal-lending-and-credit-reporting-misconduct/.

[49] James R. Hood, “Trump-Era CFPB Under Fire as $360 Million in Consumer Redress Goes Missing or Reversed,” ConsumerAffairs, July 29, 2025. https://www.consumeraffairs.com/news/trump-era-cfpb-under-fire-as-360-million-in-consumer-redress-goes-missing-or-reversed-072925.html.

[50] US Department of Transportation, “Airline Customer Service Dashboard,” n.d. https://www.transportation.gov/airconsumer/airline-customer-service-dashboard.

[51] “The Price Isn’t Right: How Junk Fees Cost Consumers and Undermine Competition,” The White House, March 4, 2024. https://bidenwhitehouse.archives.gov/cea/written-materials/2024/03/05/the-price-isnt-right-how-junk-fees-cost-consumers-and-underminecompetition/.

[52] Consumer Financial Protection Bureau, “CFPB Closes Overdraft Loophole to Save Americans Billions in Fees,” December 12, 2024. https://www.consumerfinance.gov/about-us/newsroom/cfpb-closes-overdraft-loophole-to-save-americans-billions-in-fees/.

[53] Office of the Minnesota Attorney General, “Attorney General Ellison Seeks to Protect Consumers From High Overdraft Fees,” April 10, 2025. https://www.ag.state.mn.us/Office/Communications/2025/04/10_OverdraftFees.asp.

[54] Bryan Bennett, “Majorities Support the Junk Fees Prevention Act and Raising the Debt Ceiling,” Navigator, July 24, 2023. https://navigatorresearch.org/majorities-support-thejunk-fees-prevention-act-and-raising-the-debt-ceiling/.

[55] Stephen Michael White, “How Much Does Tenant Screening Cost? Average Pricing Guide,” RentPrep, December 19, 2023. https://rentprep.com/blog/landlord-tips/how-much-does-tenant-screening-cost/-average-tenant-screening.

[56] Ben Taylor, “Who Can Drive a Rental Car? Your Guide to Additional Drivers,” Booking.com, October 16, 2025, https://www.booking.com/guides/article/cars/assigning-additional-drivers-rental-car.html.

[57] “Rental Application Fees by State,” LawDistrict, April 10, 2024. https://www.lawdistrict.com/articles/rental-application-fees-by-states.

[58] “Additional Driver Policy,” Budget, n.d. https://www.budget.com/en/help/usa-faqs/additional-driver-policy.

[59] Madison McVan, “Governor Signs ‘Junk Fee’ Ban Into Law,” Minnesota Reformer, May 20, 2024. https://minnesotareformer.com/2024/05/20/governor-signs-junk-fee-ban-intolaw/.