Innovative Research / Collaboration

Cutting Out the Middleman: A Public Option for Pharmacy Benefits

June 23, 2026

Overview

Americans pay more for prescription drugs than patients in any other wealthy country, and it's not just due to exorbitant pricing by drug manufacturers. Three corporate middlemen — CVS Caremark, Express Scripts, and OptumRx — control key channels in the drug supply chain, including roughly 80% of prescription claims in the U.S. Their business model artificially inflates and benefits from high drug prices. Government regulation and enforcement is not enough.

Executive Summary

The problem. Americans pay more for prescription drugs than patients in any other wealthy country, and it’s not just due to exorbitant pricing by drug manufacturers. Three corporate middlemen — CVS Caremark, Express Scripts, and OptumRx, collectively known as pharmacy benefit managers (PBMs) — control key channels in the drug supply chain, including roughly 80% of prescription claims in the United States. Their business model artificially inflates and benefits from high drug prices.

Why reform has failed. PBM reform has become a hot topic over the past decade but policy solutions have been woefully inadequate. Regulators have targeted well-known PBM tactics but PBMs have simply pivoted to new sources of extraction. States have passed laws just to get pre-empted in court. The big three PBMs continue to evolve faster than lawmakers legislate and enforcers litigate.

The proposal. Government regulation and enforcement is not enough. In order to fix incentives and lower costs, the market needs alternatives that don’t carry the conflicts of interests implicit in the big PBM business model. We propose a publicly operated PBM — run transparently, priced on a fee-for-service basis, and tied to a public health mission rather than to shareholder returns—serving federal employees, Medicare, Medicaid, and any commercial plan that opts in.

Why it could work. States that have shown that government can take on certain PBM functions with great success. West Virginia, for example, saves over $54 million annually on its Medicaid program and returned $120 million in revenue to independent pharmacies. The federal government already has the infrastructure to replicate this: the VA has been negotiating drug prices directly for decades and secures some of the lowest rates in the U.S. market.

What’s needed. The federal government could take immediate action to stand up a VA-based federal PBM for federal employees and military beneficiaries — roughly 18 million lives — under existing authority, without new legislation. More substantively, Congress could legislate a national public option for PBM services covering Medicare, Medicaid, and commercial plans.

Introduction

The United States is a global leader in pharmaceutical innovation, responsible for many of the world’s most important medical breakthroughs. Yet for millions of Americans, these advances remain out of reach due to the high cost of prescription drugs. One in five insured Americans and seniors, including Medicare beneficiaries, report going without needed prescriptions — skipping doses, delaying refills, or using someone else’s medication — because of cost.1 Patients with high-deductible health plans are required to pay an average of $5,456 per year before their insurance kicks in to cover their drugs.2 Unsurprisingly, polling shows that a significant majority of Americans are concerned about their ability to afford prescription drugs for themselves and their families.3 Even when insurance covers a prescription, many essential, life-saving treatments, such as cancer drugs, insulin, and autoimmune therapies, require patients to pay 20 to 50% coinsurance, amounting to thousands of dollars a month.4

Health insurers and drug manufacturers are well-documented drivers of high U.S. healthcare costs. Less recognized is the role of a fragmented pharmaceutical supply chain dominated by extractive middlemen. By some estimates, over 41% of the dollars flowing through this system go not to scientific innovation but to middlemen like PBMs, the firms that manage prescription drug benefits on behalf of insurers, employers, and other payers.5

Despite growing recognition of this problem, a decade of federal and state reform and enforcement has not curbed PBM power.6 This paper argues that to truly solve this problem and lower costs for payers and patients, what’s needed is not more patchwork regulation but a public alternative that competes directly with the Big Three PBMs (CVS Caremark, Express Scripts, and OptumRx), who hold the industry hostage. Part I explains how the Big Three broke the drug market by vertically integrating and turning every piece of the supply chain into a revenue stream tied to inflated list prices. Part II explains why traditional levers of regulation and enforcement have not worked. Finally, Part III proposes two paths for government to build its own PBM: a near-term, VA-based federal PBM under existing executive authority, and a legislated national public option open to Medicare, Medicaid, and commercial plans.

Cutting Out the Middleman: A Public Option for Pharmacy Benefits

Three corporate middlemen — CVS Caremark, Express Scripts, and OptumRx — control key channels in the drug supply chain, including roughly 80% of prescription claims in the U.S. Government regulation and enforcement is not enough.

Read the full report.

Part I: How PBMs Broke the Drug Market

What PBMs Do and How They Came to Dominate the Drug Market

PBMs have humble origins, beginning in the late 1960s as back-office claims processors created by groups of pharmacists and insurers to handle paperwork for limited prescription drug benefit programs.7 Through the 1980s and 1990s, as blockbuster drugs for chronic conditions proliferated and employers expanded drug coverage, PBMs grew into powerful intermediaries, building pharmacy networks, designing formularies, and negotiating directly with manufacturers for rebates in exchange for preferred placement on those formularies.8 Rebates, originally intended to lower costs for plans and patients, became a core revenue stream PBMs kept a growing share of.

Through the 2000s and 2010s, PBMs extended into mail-order and specialty pharmacies and consolidated aggressively. Medicare Part D, launched in 2006, routed billions of federal dollars through private PBMs. Lax antitrust oversight and the Employee Retirement Income Security Act’s (ERISA) protection against state regulation accelerated the trend: CVS acquired Caremark in 2007 and insurer Aetna in 2018; Express Scripts absorbed Medco in 2011 and was bought by Cigna; UnitedHealth built OptumRx and bought Catamaran in 2015.9

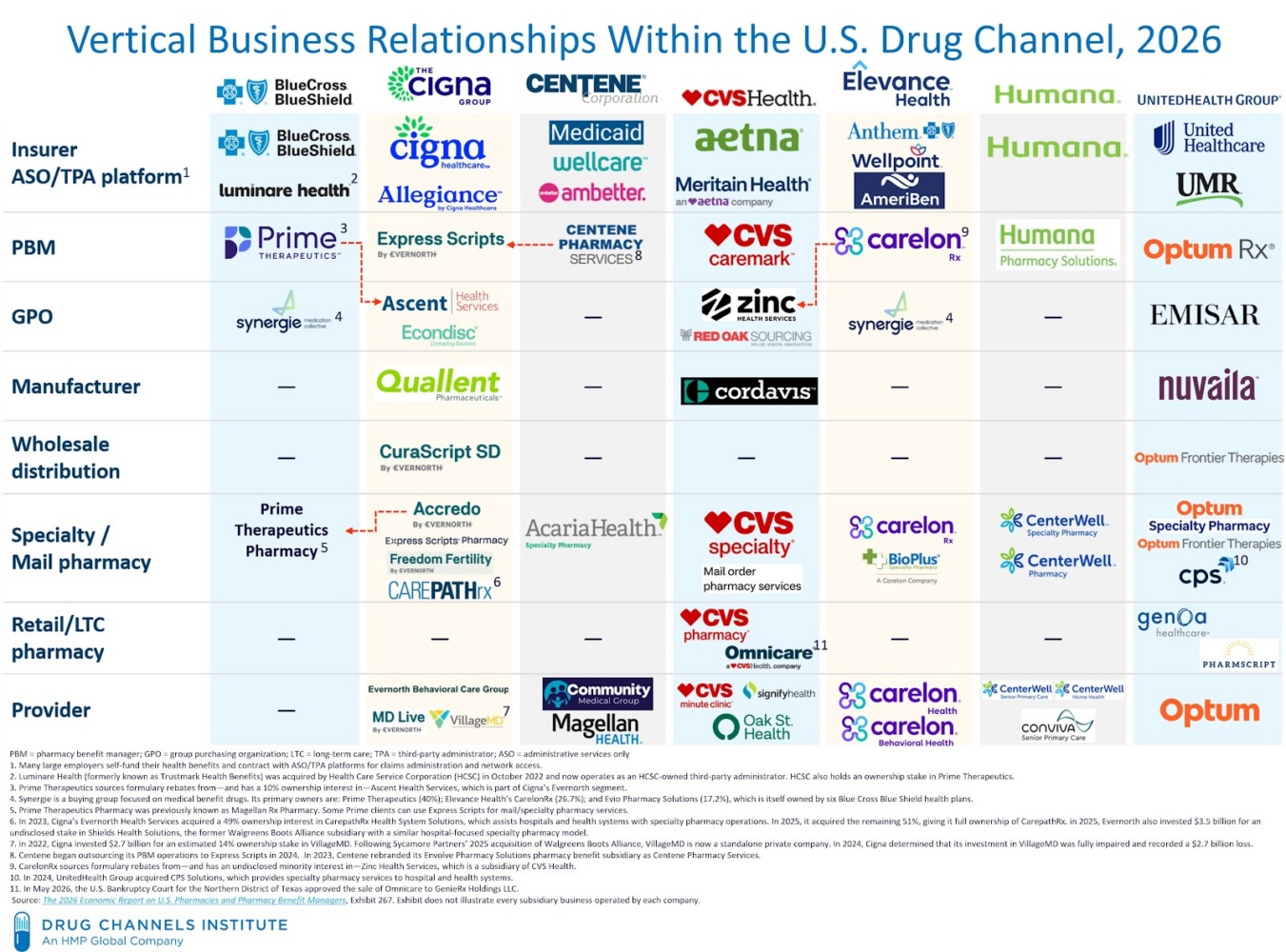

After two decades of consolidation, CVS Caremark, Express Scripts, and OptumRx grew to control approximately 80% of the market.10 As Figure 1 shows, all three major PBMs are now vertically integrated, each owned by a large health insurance company while also operating their own mail-order, specialty pharmacies, and other related businesses.

Figure 1: Vertical Business Relationships Within the U.S. Drug Market

Today, the spoils of vertical and horizontal integration allow PBMs to exert power over almost every stage of the pharmaceutical supply chain. They influence premiums for employers and unions. They determine which drugs make the formulary, which makes them de-facto kingmakers for generic and biosimilar manufacturers. They decide which pharmacies are in network and how much those pharmacies get reimbursed. They dictate what patients pay out of pocket. They even co-manufacture some drugs themselves (more on this later). This leverage lets PBMs extract fees from every participant in the prescription drug market. What was once a simple fee-for-service business model is now an unwieldy menu of direct and indirect fees, some so nonsensical even the sharpest PBM executive would struggle to explain them with a straight face. Many of these fees are buried in vague contract language and reported in bulk, leaving plan employers unable to audit pricing. Faced with limited insight into claims and few viable PBM alternatives, employers usually pass the increases to employees through higher premiums.

PBM business models have a habit of shapeshifting. Every time regulators have targeted a source of PBM extraction, a new one emerges to replace it. A decade of state and federal reform has been aimed at where the money used to be and PBMs simply moved the money.

To further protect their revenue streams, the Big Three have moved rebate negotiation offshore. Each runs it through its own captive group purchasing organization (GPO), a subsidiary of the PBM that negotiates manufacturer rebates, letting the PBM shift those flows off its own books and out of regulators’ line of sight while collecting percentage-based “administrative fees” along the way. Ascent Health Services (Switzerland) handles rebates for Express Scripts, while Emisar Pharma Services (Ireland) performs the same function for OptumRx. Although CVS Caremark has kept its GPO, Zinc Health Services, onshore, it has adopted a largely similar organizational model.11

Table 1: Non-exhaustive List of Hidden Fees Charged by PBMs or Affiliated Entities

| Fee/Charge |

Description |

Paid By |

| Rebate Retention |

PBM retains a portion of the rebate instead of passing the full amount to the plan sponsor. Often undisclosed. |

Drug Manufacturers |

| Administrative Fees (Rebate Admin) |

Charged for managing rebate negotiations and contracts. May be a flat fee or percentage of total rebates. |

Manufacturers, Plan Sponsors |

| Formulary Access/Placement Fees |

Payments to ensure a drug is included or favored on the formulary. Often bundled into rebate agreements. |

Drug Manufacturers |

| Data Access Fees |

Fees for de-identified claims or utilization data to support market access or pricing strategy. |

Drug Manufacturers |

| Fixed Participation Fees |

Entry or membership fees for manufacturers to participate in GPO-negotiated contracts. |

Drug Manufacturers |

| Non-Pass-Through Rebates |

Rebates routed through GPOs and retained or partially passed on to the plan sponsor without full disclosure. |

Drug Manufacturers |

| Spread Pricing |

PBM charges more for a drug than it reimburses the pharmacy, keeping the difference (the “spread”). |

Plan Sponsors |

| Per-Claim Fees |

Flat fees for each prescription processed, regardless of cost or value. Often buried in administrative billing. |

Plan Sponsors |

| Specialty Pharmacy Markups |

PBMs-affiliated pharmacies purchase high-cost specialty drugs at discounted prices and resell them at marked-up rates to plans, keeping the spread. These markups are often not disclosed or auditable. |

Plan Sponsors |

| Network Access Fees |

Charges for participating in preferred or limited networks, often required for volume. |

Pharmacies |

| Direct and Indirect Remuneration (DIR Fees) |

ChRetroactive fees clawed back after point-of-sale transactions, sometimes months later. |

Pharmacies |

How PBMs Profit from Inflation

What’s most problematic about the pharmaceutical industry is that PBMs, whose stated purpose is to control costs, often make more money when they place higher-priced drugs on their formularies, because many of the fees they collect across the supply chain scale with the price of the drug. Rebates, GPO administrative fees, and specialty-pharmacy margins all increase when manufacturers raise prices. The result is higher drug costs for payers, patients, and employers.

The clearest illustration of this dynamic is Humira. AbbVie’s blockbuster anti-inflammatory, used to treat rheumatoid arthritis and similar conditions, was the single most profitable drug in U.S. history for most of the last decade.12 Its list price climbed for twenty consecutive years, eventually passing $80,000 per patient per year.13

Pricing for Humira was the product of a mutually reinforcing arrangement between AbbVie and the PBMs. The PBMs benefited because each time AbbVie raised the list price, it paid larger rebates to keep Humira on preferred formularies. Some of those rebates reached insurers or employers, but much of the value was retained by the PBMs directly or captured by their corporate affiliates through the fee structures described above. AbbVie, in turn, benefited enormously, generating nearly $200 billion in revenue over Humira’s twenty-year run, while the rebate strategy helped preserve its market exclusivity by keeping biosimilar competitors off formularies.14 Everyone inside the arrangement did exceptionally well, except the patients, who were left paying deductibles and coinsurance based on an $80,000 list price.15

By some estimates, over 41% of the dollars flowing through this system go not to scientific innovation but to middlemen like PBMs, the firms that manage prescription drug benefits on behalf of insurers, employers, and other payers.

Even when Humira biosimilars began reaching the U.S. market in 2023, PBMs kept them off formularies. Through 2024, despite more than a dozen biosimilar alternatives available, Humira still accounted for roughly 70% of prescriptions for its molecule.16 The alternatives were not worse; their manufacturers could not match AbbVie’s rebate payments. The Federal Trade Commission (FTC) documented the mechanism in its 2024 interim report on PBM practices and again in its 2025 administrative complaint: a “rebate wall” — exclusive contracts in which a brand manufacturer’s rebate is conditional on competing biosimilars being kept off the preferred formulary.17

Today, biosimilars have made inroads, but PBMs have predictably found new ways to extract value. By December 2025, biosimilars accounted for more than 50% of the Humira-molecule market.18 But the products gaining share were often not those from independent manufacturers. Instead, they were PBM-owned private-label biosimilars marketed through subsidiaries the Big Three created for precisely this purpose: CVS’s Cordavis (incorporated in Ireland), Express Scripts’ Quallent Pharmaceuticals (Cayman Islands), and OptumRx’s Nuvaila (Ireland). About 60% of new Humira-equivalent prescriptions now flow through Cordavis’s product.19 It is priced roughly 81% below Humira’s original list price, yet the margin on every prescription still flows back to CVS Caremark, its affiliated specialty pharmacy, and its captive GPO. Rather than allowing biosimilar competition to lower prices as intended, PBMs restructured the market so the biosimilar transition itself became a new revenue stream.

Humira encapsulates the paper’s argument in a single drug: when the profits were in rebates, PBMs kept Humira on formulary; when the profits shifted to specialty dispensing and GPO fees, they relaunched the same molecule under their own private-label biosimilars. PBMs consistently find the gaps policymakers fail to address.

So while biosimilars have lowered costs, PBMs continue to limit the full potential of those savings. For comparison, in 2025 Cost Plus launched Starjemza, a biosimilar to the blockbuster immunology drug Stelara, at a list price roughly 99% below the Stelara reference product.20 That is what a transparent, non-PBM-mediated biosimilar market can produce. The difference between an 81% discount and a 99% discount reflects the cost of routing a biosimilar through the same intermediaries that inflated the reference drug in the first place.

Humira encapsulates the paper’s argument in a single drug: when the profits were in rebates, PBMs kept Humira on formulary; when the profits shifted to specialty dispensing and GPO fees, they relaunched the same molecule under their own private-label biosimilars. PBMs consistently find the gaps policymakers fail to address.

And beneath all this complexity and profiteering, we have to remember that it is the patient who bears the cost.

The Human Cost of PBM Dominance

Consider the case of Cole Schmidtknech. Cole was 22 years old, living in Arcadia, Wisconsin. Like millions of Americans managing chronic conditions, he was working hard to build a stable life — and relying on his insurance and pharmaceutical benefits to help him stay healthy.

For close to a decade, the medication for his chronic asthma had been covered by his insurance, with an out-of-pocket cost of less than $70. But in January 2024, when he went to Walgreens to refill his Advair Diskus inhaler, the pharmacist informed him that OptumRx, the PBM subsidiary of UnitedHealth, would no longer cover it. The price of purchasing the inhaler out-pocket would be $539. Cole received no advance notice of the change. Faced with the choice between paying rent or buying his medication, he chose rent. Five days later, he suffered a severe asthma attack, lost consciousness on the way to the hospital, and died after six days on life support.21

One year after his death, Cole’s parents filed a lawsuit against Walgreens and OptumRx. The complaint alleges that OptumRx violated state law by removing the medication from coverage without medical justification or proper notice.22 It further alleges that the coverage decision was based on a financial arrangement between OptumRx and a manufacturer, prioritizing higher-cost medications over what was best for Cole’s health. Specifically, the complaint alleges that “OptumRx would only cover Advair HFA or Breo Ellipta, two newer brand drugs, whose manufacturer had paid OptumRx substantial kickbacks (euphemistically called “rebates” and/or “compensation”) in exchange for their favorable placement on OptumRx’s updated formulary, while excluding Advair Diskus and its generic equivalents.”23

Cole’s story reflects the daily experience of countless patients across the country — a person with diabetes whose preferred insulin suddenly needs prior authorization, or an arthritis patient suddenly saddled with a $300 copay for an anti-inflammatory drug. These are the real-world consequences of a system where intermediaries make critical coverage decisions based not on clinical value, but on maximizing revenue thanks to an incentive system that rewards high prices.

Part II: Why Reform Has Fallen Short

Policymakers have long recognized these problems. Yet the response has failed to confront the structural drivers of cost or deliver relief at a meaningful scale.

Federal:

The Inflation Reduction Act marked a historic shift by allowing Medicare to negotiate the prices of a limited set of high-cost drugs.24 But the law did not address the role of pharmacy benefit managers in inflating list prices or obstructing access to generic and biosimilar alternatives.

The FTC, under the Biden Administration, initiated enforcement action against the three largest PBMs — Caremark Rx, Express Scripts, and OptumRx — and their affiliated GPOs. In February 2026, the FTC secured a settlement with Express Scripts, requiring it to stop favoring high-list-price drugs, base patient out-of-pocket costs on net drug prices, move its offshore rebate purchasing organization (Ascent Health Services) back to the United States, and operate under an independent compliance monitor for three years.25 The FTC estimates the settlement will deliver roughly $7 billion in patient savings over a decade but whether it delivers that in practice is an open question.

The Consolidated Appropriations Act of 2026, signed into law on February 3, 2026, enacted the most significant federal PBM legislation to date.26 It requires Medicare Part D PBMs to charge flat administrative fees and pass through all manufacturer rebates, while adding new reporting requirements and an “any willing pharmacy” rule.27 These are meaningful changes — but they apply only to Medicare, leave commercial plans untouched, and will not be fully implemented until 2028–2029.

The Trump administration has also taken steps on drug pricing, including executive orders on PBM transparency and “Most Favored Nation” pricing, along with voluntary agreements with drug manufacturers.28 But these measures do not address the underlying PBM rebate system, fees, or pricing practices that can significantly increase what patients pay at the pharmacy counter.

State:

In 2024, 20 states enacted 33 bills aimed at regulating PBMs, ranging from laws targeting shady fees and spread pricing.29 But most of these reforms are narrowly tailored, often limited to Medicaid markets or a specific subset of PBM activities.

And when states have been aggressive, they’ve been blocked by courts. Arkansas passed a groundbreaking law banning PBMs from owning or operating pharmacies in the state, a move designed to eliminate structural conflicts of interest. However, in July 2025, a federal judge issued a preliminary injunction, citing likely violations of the Commerce Clause.30 Tennessee is considering a similar bill and that would likely face similar challenges in court.31

In May of this year, Iowa passed sweeping PBM regulation aimed at transparency, network composition, and pharmacy choice. In July, this reform was also blocked, with a federal court issuing a preliminary injunction, finding that key provisions were likely preempted by ERISA and violated the First Amendment by restricting commercial speech.32 Like the Arkansas case, this showdown highlights how legal constraints derail state-level attempts to rein in PBM practices.

Private:

New entrants like Mark Cuban’s Cost Plus Drugs Drug Company (MCCPDC) and Amazon’s Rx Pass aim to bypass intermediaries entirely by purchasing drugs directly from manufacturers and selling them to cash-paying consumers through online pharmacies. These initiatives have shown promise, delivering significant savings on select medications and illustrating just how much PBM markups inflate prices at the pharmacy counter.33

Yet their impact remains limited. First, these models primarily serve uninsured patients or those with high-deductible health plans, since partnering with insurance plans requires working through PBMs and, consequently, accepting their pricing structure. Second, and more fundamentally, the drugs offered through these platforms are almost entirely off-patent generics, which are already relatively affordable. In fact, generic drugs in the U.S. are, on average, priced 33% lower than in other OECD countries.34 Meanwhile, the top ten drugs by Medicare spending are all brand-name medications — precisely the segment where price inflation is most acute.35

In recent years, a wave of “transparent PBMs” have also entered the market. They offer basic PBM services without the hidden fees and profit-seeking tactics associated with the vertically integrated giants. Companies like AffirmedRx and Navitus Health Solutions offer 100% pass-through pricing, flat-fee compensation models (“delinking”), and technology that enables data sharing across patients, insurers, pharmacists, and other stakeholders.36 These measures have the potential to reduce costs for both plans and patients. For example, one transparent PBM reports that it can lower the cost per claim of oral beta blockers used to treat high blood pressure by 90% compared to traditional PBM pricing.37

While these models are promising, transparent PBMs have yet to achieve the scale needed to meaningfully disrupt the dominance of Caremark, Express Scripts and OptumRx. Nearly three-quarters of employers still contract with a “big three” PBMs and only 12% work with a smaller transparent PBM.38

Neither regulation nor private competition has curbed the excesses of PBM power. Part of the reason is incentives: despite growing criticism, governments and employers continue to pay PBMs enormous sums, leaving little market pressure to change and giving new entrants few opportunities to compete.39 Reformers have also missed the mark. While well-meaning, many remain focused on outdated issues like spread pricing and rebates, even as PBMs evolve, create new revenue streams, and reorganize to stay ahead of oversight.

Part III: A Public Option for PBM Services

To meaningfully reform the pharmaceutical supply chain, we propose that the federal government, in partnership with states, create its own democratically accountable PBMs, in direct competition with private PBMs in federal healthcare benefits, state employer and Medicaid programs, and commercial insurance markets. Critically, the public PBM would also publish negotiated prices for each drug in its formulary, a vital step towards restoring transparency, accountability, and affordability at scale.

State Evidence: Public PBMs Already Work at Smaller Scale

Public provisioning of PBM services is not new. It just hasn’t been done systematically or at scale. At the state level, a growing number of states have already begun reclaiming democratic control over pharmacy benefit services.

Most state approaches stop short of creating a full public PBM but they prove that a direct government role in the provision of PBM services can produce cost savings and transparency gains.

West Virginia:

West Virginia led the way in 2017 by carving pharmacy benefits out of its Medicaid managed care program.40 By assuming direct control over purchasing and benefit management, the state saved over $54 million annually, eliminated spread pricing, and improved oversight of rebate flows. Maybe more salient for lawmakers, it also meant that local West Virginia community pharmacies made over $120 million more in revenue because they got fair prices and weren’t facing extraction from the Big Three.

Ohio:

Following West Virginia’s lead, Ohio conducted an audit of its Medicaid pharmacy program in 2018, which found that PBMs were charging the state far above what they reimbursed pharmacies. In response, Ohio implemented a single, transparent PBM contract model in 2022, awarding the contract to a vendor operating on a pass-through pricing basis and with strict data reporting requirements.41 The new structure gave the state better control over formulary design and pharmacy reimbursements while eliminating opaque PBM profit-taking.

Kentucky:

Kentucky also took steps to reform its Medicaid PBM practices after discovering significant pricing discrepancies and complaints from independent pharmacies.42 In 2021, the state enacted legislation mandating the transition to a single-PBM model under state oversight.43 The move was designed to increase transparency, reduce administrative complexity, and stop PBMs from leveraging vertical integration to direct patients toward affiliated pharmacies.

Indiana:

Indiana recently passed PBM legislation that, among its provisions, establishes reimbursement floors for pharmacies in the commercial market and imposes new guardrails on PBM pharmacy networks.44 An early version of the bill included a provision to create a state-owned PBM that would serve all state plans, including Medicaid and state employee health programs.45 But a surge of PBM lobbying watered down the promising provision.

ArrayRx:

More ambitious is ArrayRx, a joint effort by Arizona, Oregon, Washington, Nevada, and Connecticut designed to centralize and coordinate critical pharmacy benefit functions, including drug price negotiations, claims processing, and pharmacy network management, under a transparent, publicly accountable framework.46 By pooling their purchasing power, these states negotiate larger rebates, all while operating under a transparent, pass-through pricing model that eliminates spread pricing and hidden fees. In doing so, ArrayRx functions as a quasi-public PBM, demonstrating that states can not only administer pharmacy benefits directly but can also collaborate regionally to increase leverage, improve accountability, and deliver lower costs to patients. Originally launched as the Oregon Prescription Drug Program, ArrayRx has expanded its model to other states seeking alternatives to opaque, profit-driven PBM practices.

Federal Pathway: Two Models

What transparent PBM startups and state-level efforts lack is scale. PBMs like Express Scripts cover 100 million lives, and matching that purchasing power requires coordination.

The federal government is the obvious place to build that scale. A federal PBM could offer a single alternative to the large, vertically integrated PBMs and make it available to any plan sponsor in the country. There are several ways to do this, ranging from options that rely on existing executive authority to more expansive models that would require new legislation.

Model 1: Public PBM for Federal Employees

The first option for a federal PBM could be implemented under existing legal authority, without new legislation. This model would initially focus on serving federal employees and beneficiaries within the FEHB and TRICARE programs.

The Federal Employees Health Benefits (FEHB) Program is the largest employer-sponsored health insurance program in the country, providing more than $40 billion in health care benefits annually to employees and retirees of the federal government, the largest employer in the United States.47 Today, the FEHB contracts out management of health benefits to private insurance plans that, in turn, subcontract pharmacy benefit management services to private PBMs (usually their own vertically integrated PBM).

Similarly, TRICARE, the Department of Defense’s health insurance program, covers approximately 9.6 million beneficiaries, including active-duty service members, their families, retirees, and eligible survivors.48 The program spends over $8 billion annually on prescription drugs and operates through two main components: a direct purchasing program, where drugs are dispensed at military treatment facilities (MTFs), and a mail and retail pharmacy program.49

To meaningfully reform the pharmaceutical supply chain, we propose that the federal government, in partnership with states, create its own democratically accountable PBMs, in direct competition with private PBMs in federal healthcare benefits, state employer and Medicaid programs, and commercial insurance markets.

Like FEHB, TRICARE contracts out its mail and retail pharmacy benefit services to Express Scripts, one of the big three PBMs. Express Scripts has administered TRICARE’s pharmacy benefits since 2009 and, in 2021, was awarded a new eight-year contract worth up to $4.3 billion, not including the cost of the drugs themselves.50 While TRICARE’s direct procurement model achieves relatively low drug costs, the Express Scripts–managed retail pharmacy program has been shown to result in higher average unit prices for both brand-name and generic drugs compared to the Department of Veterans Affairs (VA).51

While FEHB is required by statute to contract its services out, it can legally contract it out to another government entity. The VA has tremendous experience negotiating drug prices across multiple programs. Its Pharmacy Benefits Management Services section already sets up and manages a national formulary and operates a pharmacy network for 9 million veterans.52 Likewise, its National Acquisition Center manages the Federal Supply Schedule for pharmaceuticals, known as Schedule 65IB, negotiating multi-year, multiple-award contracts directly with drug manufacturers to secure fixed prices that are among the lowest in the U.S. market.53

The Office of Personnel Management (OPM) could change the eligibility requirement in its contracts such that only an entity performing at the VA PBM’s level qualifies to provide the services, meaning that either the VA gets the contract, or one of the Big Three PBMs after reforming their practices to minimize the value they siphon off through rebates and other practices.54

The VA’s prices would serve as the baseline for negotiations, with pharmacies reimbursed through a transparent cost-plus model — eliminating spread pricing, hidden rebates, and incentives that reward high list prices. Publishing these prices would also pressure private PBM negotiations toward greater transparency.

Figure 2: Proposed Model 1 (FEHM, TRICARE)

While an option that doesn’t rely on Congress is appealing, the VA-based approach applies largely to drug purchasing for federal employees and excludes other major government programs like Medicaid, Medicare, and Affordable Care Act (ACA) marketplace exchanges. To achieve a meaningful impact on drug prices nationwide, a more expansive solution is needed: the creation of a unified federal prescription drug contracting program, a broader program that would require congressional authorization and dedicated funding.

Similar to the VA-based model for federal employees, the unified program would run its own national formulary and perform core PBM functions in-house, including drug-price negotiation, claims adjudication, and pharmacy-network management. It would also operate with transparent, fixed pricing, eliminating rebates and other opaque payment structures. As its name suggests, this federal PBM would span Medicare, Medicaid, TRICARE, and FEHB, serving different functions for each program:

- In FEHB and TRICARE, the federal PBM would become the sole administrator for federal employees and beneficiaries.

- In Medicare Part D and Medicare Advantage, the federal PBM would compete with private PBMs, bidding for market share as an alternative plan sponsor.

- In Medicaid, the federal PBM would be made available to states (including those that have carved PBMs out of their Medicaid programs), offering optional support in claims processing, rebate negotiation, and pharmacy network oversight. This would probably require some restructuring of Medicaid Drug Rebate and 340B programs.

Perhaps most importantly, it would be open to all health plans in the United States. Commercial insurers, both in employer and ACA exchange markets, that contract private PBMs could opt in to use the federal PBM’s services and pricing framework. It would also contain similar drug level transparency requirements, so even those insurers who did not join the PBM could see the pricing structure that is available under its negotiations.

Figure 3: Proposed Model 2 (Medicare and Medicaid)

Governance and Implementation

We argue that the most effective path is to establish a quasi-public institution that combines public oversight with operational independence. One example is the National Semiconductor Technology Center (NSTC), established under the CHIPS and Science Act of 2022.55 It was overseen by a federal board but operated by an independent, nonprofit entity that could engage directly with industry, manage intellectual property, and respond rapidly to technological and market shifts.

This entity could be governed by a board composed of all relevant federal health care payers, including the U.S. Department of Health and Human Services (HHS), FEHB, VA, and TRICARE, ensuring alignment with national health priorities. One agency, likely HHS, would take the lead on oversight and contribute a greater share of resources, as the Department of Commerce does with the NSTC, but the public PBM itself would act as a flexible, independent public corporation, free from the bureaucratic constraints of any single agency.

Considering that PBMs had the highest profit margins among all intermediaries in the pharmaceutical supply chain, with $60.6 billion in profits in 2022, reducing their market share would be a rare policy intervention that delivers cost savings to both taxpayers and patients across public and private insurance markets.56

This model should also include statutory authority to operate in the commercial insurance market as an optional PBM for private plans. By leveraging the scale of its core government contracts, the federal PBM would have sufficient market presence to serve as a consistent and credible alternative, essentially a maverick player capable of offering transparent, cost-effective services to private employers, unions, and health plans that choose to opt in.

Considering that PBMs had the highest profit margins among all intermediaries in the pharmaceutical supply chain, with $60.6 billion in profits in 2022, reducing their market share would be a rare policy intervention that delivers cost savings to both taxpayers and patients across public and private insurance markets.

Both models would be fee-for-service and consequently also revenue neutral, or even slightly profitable. The current private versions of PBM services are wildly profitable which suggests that a federal or state option would be able to provide fair and consistent services at a significantly lower cost without spending taxpayer dollars. They may even be net contributors to the federal budget, though any reform should not seek to replace private monopoly pricing with public monopoly pricing.

Conclusion

In the U.S., the core problem with PBMs lies in their incentives, market power, and scale—all deployed to keep prices high and extract revenue rather than deliver value. A public PBM would not solve every problem in the healthcare system, but it could achieve meaningful cost savings and improve the experience for patients, pharmacists, and manufacturers.

We have floundered for years attempting to fix the drug market while relying on the tired ideology of privatization. But to fix drug negotiation markets, we need to invest in democratically accountable institutions with the power to deliver for the people, not put more faith in the private corporate model that has failed us time and again.

Appendix A: A Brief Roadmap for State Policymakers

Federal legislation remains the most scalable path to break the Big Three’s grip on the pharmaceutical market. But state action delivers savings now, builds political constituencies for federal reform, and continues to matter even once a federal public option is established. States considering independent action have a number of tools and authorities at their disposal. The recommendations below consolidate what has worked in West Virginia, Ohio, Kentucky, Indiana, and the ArrayRx coalition.

Transition from managed care to fee-for-service. States should move Medicaid pharmacy benefits from managed-care capitation to a fee-for-service carve-out administered directly by the state. Managed-care arrangements bury PBM fees inside per-member-per-month payments that the state cannot audit. Fee-for-service creates the transparency baseline every other reform depends on. Ohio’s 2022 transition to a single fee-for-service contract administered by Gainwell delivered roughly $140 million in first-year savings.57

Pool purchasing power across state agencies. Most states operate multiple separate drug-purchasing streams — Medicaid, state employees and retirees, corrections, state university systems, community colleges, and participating counties and K–12 districts. Consolidating these into a single purchasing entity gives the state leverage closer to that of a mid-sized PBM.

Use an accountable public institution for formulary decisions. States should route formulary management through an existing public body — a state university school of pharmacy, an independent board of clinicians, or a state pharmacy commission — rather than a contracted PBM. West Virginia’s decision to route formulary management and prior authorization through WVU School of Pharmacy is the cleanest precedent.58 It keeps drug-coverage decisions grounded in clinical judgment rather than rebate economics.

Allow commercial plans to opt in. Once a state has stood up a transparent public PBM function, it should allow private employers and commercial plans in the state to buy in for a low, fixed administrative fee. Opt-in expands the subscriber base, increases negotiating leverage, and solves the scale problem that has kept standalone transparent PBMs from competing with the Big Three.

Coordinate across state lines. Individual states plateau at a few million covered lives; that cap is the reason state reforms deliver real but bounded savings. Interstate coalitions on the ArrayRx model — currently Oregon, Washington, Nevada, and Connecticut — give smaller states leverage approaching a regional PBM’s. There are no prohibitive federal barriers to states offering PBM services across state lines, and multi-state compacts can be authorized by legislation or executive compact.

Authors

Alejandro Molina is currently a Fellow at Groundwork Collaborative and Chief Operating Officer of an early-stage technology company. He served in the Biden Administration as Director of Economic Policy at the White House National Economic Council, where he led cross-agency efforts to improve competition in healthcare markets and advance industrial policy initiatives including the expansion of broadband internet and electric vehicle manufacturing. Before that, Alejandro worked at Deloitte Consulting, where he advised federal health agencies on operational strategy — improving the impact of major grant programs. He brings a mix of policy expertise and operational know-how, with an MBA from Harvard and a BA in Computer Science from Brown.

Reed Showalter is a Senior Fellow at the Vanderbilt Policy Accelerator (VPA). He is an antitrust attorney and economic justice advocate. He previously served as an attorney at the Department of Justice, Federal Trade Commission, and on the White House National Economic Council. His work focuses on reimagining progressive government to disrupt concentrated economic power and affirmatively act in markets.

Acknowledgements

Authors would like to thank: Luke Slindee, Dana Brown, Ganesh Sitaraman, Hannah Garden-Monheit, David Barclay, Hayden Rooke-Ley, and John Gray for their insight and input.

Endnotes

[1] Grace Sparks, Lunna Lopes, Alex Montero, Marley Presiado, and Liz Hamel, “Americans’ Challenges with Health Care Costs,” KFF, April 30, 2026, https://www.kff.org/health-costs/americans-challenges-with-health-care-costs/; Julie Carter, “Study Finds Older Adults Skipping Medications Due to Cost,” Medicare Watch, May 25, 2023, https://www.medicarerights.org/medicare-watch/2023/05/25/study-finds-older-adults-skipping-medications-due-to-cost.

[2] KFF, 2023 “Employer Health Benefits Survey,” October 18, 2023, https://www.kff.org/report-section/ehbs-2023-section-8-high-deductible-health-plans-with-savings-option/.

[3] KFF, “Poll: Public Worries About Prescription Drug Costs Reach New High; Most Across Political Parties Want Government to Do More to Regulate Prices” March 13, 2026. https://www.kff.org/public-opinion/poll-public-worries-about-prescription-drug-costs-reach-new-high-most-across-political-parties-want-government-to-do-more-to-regulate-prices/.

[4] KFF, 2025 Employer Health Benefits Survey, October 22, 2025, sec. 9, “Prescription Drug Benefits,” under “Separate Tiers for Specialty Drugs,” https://www.kff.org/health-costs/2025-employer-health-benefits-survey/.

[5] Neeraj Sood, Tiffany Shih, Karen Van Nuys, and Dana Goldman, “Flow of Money Through the Pharmaceutical Distribution System,” USC Schaeffer Center for Health Policy & Economics, June 6, 2017, https://schaeffer.usc.edu/research/flow-of-money-through-the-pharmaceutical-distribution-system/.

[6] Since 2016, all 50 states have enacted PBM laws, but the Federal Trade Commission (FTC) reported in 2024 that the top three PBMs still processed nearly 80% of U.S. prescriptions and that PBM concentration and vertical integration give the largest firms significant power over drug access, pricing, and pharmacy choice. National Academy for State Health Policy, “State Action on PBMs to Address Prescription Drug Pricing,” updated July 24, 2023, https://nashp.org/state-action-on-pharmacy-benefits-managers-pbms-to-address-prescription-drug-pricing/; Federal Trade Commission, Pharmacy Benefit Managers: The Powerful Middlemen Inflating Drug Costs and Squeezing Main Street Pharmacies; Interim Staff Report (Washington, DC: Federal Trade Commission, July 2024), https://www.ftc.gov/reports/pharmacy-benefit-managers-staff-report.

[7] Robin J. Strongin, The ABCs of PBMs, Issue Brief No. 749 (Washington, DC: National Health Policy Forum, October 27, 1999), https://www.ncbi.nlm.nih.gov/books/NBK559746/.

[8] Federal Trade Commission, Pharmacy Benefit Managers: The Powerful Middlemen Inflating Drug Costs and Squeezing Main Street Pharmacies; Interim Staff Report (Washington, DC: Federal Trade Commission, July 2024), https://www.ftc.gov/reports/pharmacy-benefit-managers-staff-report.

[9] Our History,” CVS Health, accessed May 31, 2026, https://www.cvshealth.com/about/our-strategy/company-history.html; Adam J. Fein, “The Cigna-Express Scripts Deal’s Intriguing Connections With — And Implications For — AmerisourceBergen and Walgreens,” Drug Channels, September 25, 2018, https://www.drugchannels.net/2018/09/the-cigna-express-scripts-deals.html; Eric Sagonowsky, “Catamaran and OptumRx to Combine,” FiercePharma, March 31, 2015, https://www.fiercepharma.com/pharma/catamaran-and-optumrx-to-combine.

[10] Adam J. Fein, “The Top Pharmacy Benefit Managers of 2024: Market Share and Key Industry Developments,” Drug Channels (blog), March 31, 2025, https://www.drugchannels.net/2025/03/the-top-pharmacy-benefit-managers-of.html.

[11] Adam J. Fein, “Five (or Maybe Six?) Reasons that the Largest PBMs Operate Group Purchasing Organizations,” Drug Channels, May 9, 2023, https://www.drugchannels.net/2023/05/five-or-maybe-six-reasons-that-largest.html.

[12] David Wainer, “What a $200 Billion Blockbuster Drug Reveals About Big Pharma’s Playbook,” Wall Street Journal, February 5, 2024, https://www.wsj.com/health/pharma/what-a-200-billion-blockbuster-drug-reveals-about-big-pharmas-playbook-e8d917c3.

[13] David Barker, Tom O’Hara, and Jamie Ross, “Biosimilars: One Answer to Cheaper Healthcare,” GAM Investments European Equities Blog, November 7, 2025, https://www.gam.com/en/our-thinking/european-equities-blog/biosimilars-one-answer-to-cheaper-healthcare.

[14] Dan Gorenstein and Leslie Walker, “AbbVie’s Blockbuster Drug Humira Finally Loses Its 20-Year, $200 Billion Monopoly,” NPR, January 31, 2023, https://www.npr.org/sections/health-shots/2023/01/31/1152513058/abbvies-blockbuster-drug-humira-finally-loses-its-20-year-200-billion-monopoly.

[15] Rebecca Robbins, “How a Drug Company Made $114 Billion by Gaming the U.S. Patent System,” New York Times, January 28, 2023, https://www.nytimes.com/2023/01/28/business/humira-abbvie-monopoly.html.

[16] Biosimilars Council, “Humira Biosimilar Landscape: Still Waiting,” January 30, 2024, https://biosimilarscouncil.org/resource/humira-biosimilar-landscape-still-waiting/.

[17] Federal Trade Commission, “Pharmacy Benefit Managers: The Powerful Middlemen Inflating Drug Costs and Squeezing Main Street Pharmacies,” July 2024, https://www.ftc.gov/reports/pharmacy-benefit-managers-report.

[18] Evernorth Research Institute, “Pharmacy in Focus: The Biosimilar Breakthrough in Adoption and Affordability,” (Evernorth Health Services, 2025), https://www.evernorth.com/sites/default/files/2025-08/2025%20Pharmacy%20in%20Focus%20Biosimilars%20Report.pdf.

[19] Adam J. Fein, “Humira Biosimilar Price War Update: Should We Be Glad that CVS Health and Express Scripts Are Using Private Label Products to Pop the Gross-to-Net Bubble?” Drug Channels, September 4, 2024, https://www.drugchannels.net/2024/09/humira-biosimilar-price-war-update.html.

[20] Adam J. Fein, “Drug Channels News Roundup, November 2025: PBM Revolution, Cuban’s Stelara Challenge, Express Scripts’ Price Games, U.S. Drug Spending Reality, and the AFP Reckoning,” Drug Channels, November 18, 2025, https://www.drugchannels.net/2025/11/drug-channels-news-roundup-november.html.

[21] Jason Kane, Anne Thompson, and Linda Carroll, “Parents Sue over Son’s Asthma Death Days after Inhaler Price Soared without Warning,” NBC News, June 2, 2025, https://www.nbcnews.com/health/health-care/asthma-death-prescription-price-pharmacy-lawsuit-rcna210075.

[22] Schmidtknecht v. OptumRx, Inc., No. 1:25-cv-00093 (E.D. Wis., filed Jan. 21, 2025), https://www.documentcloud.org/documents/25503515-schmidtknecht-v-optum-rx-and-walgreens/.

[23] Schmidtknecht v. OptumRx, Inc 5.

[24] Inflation Reduction Act of 2022, Pub. L. No. 117-169, §§ 11001–11002, 136 Stat. 1818, 1833–54 (2022).

[25] Federal Trade Commission, “FTC Secures Landmark Settlement with Express Scripts to Lower Drug Costs for American Patients,” press release, February 4, 2026, https://www.ftc.gov/news-events/news/press-releases/2026/02/ftc-secures-landmark-settlement-express-scripts-lower-drug-costs-american-patients.

[26] National Community Pharmacists Association, “NCPA Cheers as Trump Signs First Major PBM Reform in Decades,” press release, February 3, 2026, https://ncpa.org/newsroom/news-releases/2026/02/03/ncpa-cheers-trump-signs-first-major-pbm-reform-decades.

[27] Under Medicare Part D’s “any willing pharmacy” provision, a plan sponsor must let any pharmacy that accepts the plan’s standard terms and conditions join its network. The sponsor cannot shut out a qualified pharmacy just for not being a preferred or affiliated pharmacy. The rule protects pharmacy access and choice, though PBM-affiliated plans can still steer volume to their own pharmacies via cost-sharing and “preferred” tiers, which this floor does not bar. See Social Security Act § 1860D-4(b)(1)(A), 42 U.S.C. § 1395w-104(b)(1)(A).

[28] Donald J. Trump, “Lowering Drug Prices by Once Again Putting Americans First,” Exec. Order No. 14273, April 15, 2025, https://www.whitehouse.gov/presidential-actions/2025/04/lowering-drug-prices-by-once-again-putting-americans-first/; Donald J. Trump, “Delivering Most-Favored-Nation Prescription Drug Pricing to American Patients,” Exec. Order No. 14297, May 12, 2025, https://www.whitehouse.gov/presidential-actions/2025/05/delivering-most-favored-nation-prescription-drug-pricing-to-american-patients/.

[29] Lisa Kimbrough, “State PBM Reform: How States Are Trying to Control Pharmaceutical Spending,” MultiState, January 6, 2025, https://www.multistate.us/insider/2025/1/6/state-pbm-reform-how-states-are-trying-to-control-pharmaceutical-spending.

[30] Tess Vrbin, “Federal Judge Blocks Arkansas’ Restrictions on Pharmacy Benefit Managers,” Arkansas Advocate, July 28, 2025, https://arkansasadvocate.com/2025/07/28/federal-judge-blocks-arkansas-restrictions-on-pharmacy-benefit-managers/.

[31] National Community Pharmacists Association, “Tennessee Bill Targets PBMs’ Ownership of Pharmacies,” press release, March 3, 2026, https://ncpa.org/newsroom/qam/2026/03/03/tennessee-bill-targets-pbms-ownership-pharmacies.

[32] Robin Opsahl, “Portions of Iowa’s Pharmacy Benefit Manager Law Blocked as Lawsuit Advances,” Iowa Capital Dispatch, July 22, 2025, https://iowacapitaldispatch.com/2025/07/22/portions-of-iowas-pharmacy-benefit-manager-law-blocked-as-lawsuit-advances/.

[33] Hussain S. Lalani et al., “Potential Medicare Part D Savings on Generic Drugs from the Mark Cuban Cost Plus Drug Company,” Annals of Internal Medicine 175, no. 8 (2022): 1163–65, https://www.acpjournals.org/doi/10.7326/M22-0756.

[34] Andrew W. Mulcahy et al., International Prescription Drug Price Comparisons: Estimates Using 2022 Data (Santa Monica, CA: RAND Corporation, 2024), https://www.rand.org/pubs/research_reports/RRA788-3.html.

[35] Juliette Cubanski and Tricia Neuman, “A Small Number of Drugs Account for a Large Share of Medicare Part D Spending,” KFF, https://www.kff.org/medicare/a-small-number-of-drugs-account-for-a-large-share-of-medicare-part-d-spending/.

[36] AffirmedRx, https://affirmedrx.com/.

[37] Transparency-Rx, https://transparency-rx.com/.

[38] Matthew Gibbs, “Industry Voices — Why the Great Unraveling of PBMs Will Accelerate in 2025,” Fierce Healthcare, January 14, 2025, https://www.fiercehealthcare.com/payers/industry-voices-why-great-unraveling-pbms-will-accelerate-2025.

[39] Delaware’s state Medicaid program, for example, requires bidders to have been operating with several hundred thousand people covered for over five years, and has at least 10 other clients of the same scale as the state. Entry barriers and incentives like this make it unlikely a startup PBM can ever attain the scale needed to legitimately challenge the dominant, vertically integrated players. State of Delaware, Department of Human Resources, Statewide Benefits Office, “Request for Proposal for Pharmacy Benefit Management Services,” RFP No. DHR21002-Rx_PBM (Dover, DE: State Employee Benefits Committee, June 1, 2020), https://bidcondocs.delaware.gov/DHR/DHR_21002PharmacyBenefit_rfp.pdf.

[40] National Community Pharmacists Association, “West Virginia Medicaid Saves $54.4 Million with Prescription Drug Carve-Out,” press release, March 13, 2019, https://ncpa.org/newsroom/news-releases/2019/03/13/west-virginia-medicaid-saves-%2454.4-million-with-prescription-drug-carve-out.

[41] “As New Medicaid Prescription Program Nears, Some Ohio Pharmacists Are Worried,” Ohio Capital Journal, August 9, 2022, https://ohiocapitaljournal.com/2022/08/09/as-new-medicaid-prescription-program-nears-some-ohio-pharmacists-are-worried/.

[42] Ed Silverman, “Kentucky Probes Pharmacy Benefit Managers for Allegedly Overcharging State Medicaid,” STAT News, March 22, 2019, https://www.statnews.com/pharmalot/2019/03/22/medicaid-pharmacy-benefit-manager-kentucky-probe/.

[43] Deborah Yetter, “Reprieve for Kentucky’s Independent Pharmacies Is Saving Medicaid Millions,” Kentucky Lantern, October 5, 2023, https://kentuckylantern.com/2023/10/05/reprieve-for-kentuckys-independent-pharmacies-is-saving-medicaid-millions/.

[44] Indiana Senate Bill 140, Pharmacy Benefits, 2025 Reg. Sess., Pub. L. No. 189 (2025), https://iga.in.gov/legislative/2025/bills/senate/140/details.

[45] Abigail Ruhman, “Lawmakers Want Indiana to Own Its Own Pharmacy Benefit Manager for State Plans Like Medicaid,” WFYI Public Media, February 6, 2025, https://www.wfyi.org/health/2025-02-06/lawmakers-want-indiana-to-own-its-own-pharmacy-benefit-manager-for-state-plans-like-medicaid.

[46] Gloria Rebecca Gomez, “Hobbs Signs Order for Statewide Prescription Drug Discount Program,” Arizona Mirror, August 6, 2025, https://azmirror.com/briefs/hobbs-signs-order-for-statewide-prescription-drug-discount-program/.

[47] Ryan J. Rosso and Ada S. Cornell, “Federal Employees Health Benefits (FEHB) Program: An Overview,” CRS Report R43922, Congressional Research Service, https://www.congress.gov/crs-product/R43922.

[48] U.S. Government Accountability Office, “Defense Health Care: DOD Should Improve Monitoring of TRICARE Beneficiaries’ Access to Prescription Drugs,” GAO-25-107187 (Washington, D.C.: GAO, February 2025), https://www.gao.gov/products/gao-25-107187.

[49] GAO, Defense Health Care, GAO-25-107187.

[50] GAO, Defense Health Care, GAO-25-107187.

[51] Congressional Budget Office, “A Comparison of Brand-Name Drug Prices Among Selected Federal Programs,” (Washington, D.C.: CBO, February 2021), https://www.cbo.gov/publication/57007; U.S. Government Accountability Office, “Prescription Drugs: Comparison of DOD and VA Direct Purchase Prices,” GAO-13-358 (Washington, D.C.: GAO, May 2013), https://www.gao.gov/assets/gao-13-358.pdf.

[52] Sherrie L. Aspinall, Mariscelle M. Sales, Chester B. Good, et al., “Pharmacy Benefits Management in the Veterans Health Administration Revisited: A Decade of Advancements, 2004–2014,” Journal of Managed Care & Specialty Pharmacy 22, no. 9 (September 2016): 1058–63, https://pmc.ncbi.nlm.nih.gov/articles/PMC10398159/.

[53] U.S. Department of Veterans Affairs, “Schedule 65 I B: Drugs, Pharmaceuticals, & Hematology Related Products,” Office of Procurement, Acquisition and Logistics, https://www.va.gov/opal/nac/fss/pharmaceuticals.asp.

[54] The Economy Act (31 U.S.C. 1535) allows OPM to give this contract to the VA if it shows VA’s service is in the Government’s best interest and cheaper or more convenient than private PBMs, which should be a low bar in this market. The VA would book the revenue in its Franchise Fund, which allows it to sell business services to “other government agency customers” on a fee-for-service basis. TRICARE’s on the other hand has a broad statutory mandate to “establish an effective, efficient, integrated pharmacy benefits program” and should have clear authority to contract with the VA. 10 U.S.C. § 1074g; U.S. Department of Veterans Affairs, “Franchise Fund,” accessed June 2, 2026, https://www.va.gov/FUND/About_the_VA_Franchise_Fund.asp.

[55] Mitch Ambrose, “National Semiconductor Technology Center Taking Shape,” FYI: Science Policy News, American Institute of Physics, February 9, 2024, https://www.aip.org/fyi/national-semiconductor-technology-center-taking-shape.

[56] Eastern Research Group, Inc., “Pharmaceutical Supply Chain Intermediary Margins in the Retail Channel,” prepared for the U.S. Department of Health and Human Services, Office of the Assistant Secretary for Planning and Evaluation (Washington, D.C.: ASPE, January 14, 2025), https://aspe.hhs.gov/reports/margins-retail-channel.

[57] Marty Schladen, “Ohio Medicaid Got Rid of Big Middlemen, Paid Pharmacies More and Saved $140 Million, Report Says,” Ohio Capital Journal, April 17, 2025, https://ohiocapitaljournal.com/2025/04/17/ohio-medicaid-got-rid-of-big-middlemen-says-it-paid-pharmacies-a-lot-more-and-saved-140m/.

[58] “What Is RDTP?,” WVU School of Pharmacy, Rational Drug Therapy Program, accessed June 2, 2026, https://pharmacy.hsc.wvu.edu/rdtp/what-is-rdtp/.